- A Comprehensive Problem John And Ellen Brite Are Married File A Joint Return And Are Less Than 65 Years Old They Have 1 (63.95 KiB) Viewed 62 times

- A Comprehensive Problem John And Ellen Brite Are Married File A Joint Return And Are Less Than 65 Years Old They Have 2 (14.62 KiB) Viewed 62 times

- A Comprehensive Problem John And Ellen Brite Are Married File A Joint Return And Are Less Than 65 Years Old They Have 3 (23.78 KiB) Viewed 62 times

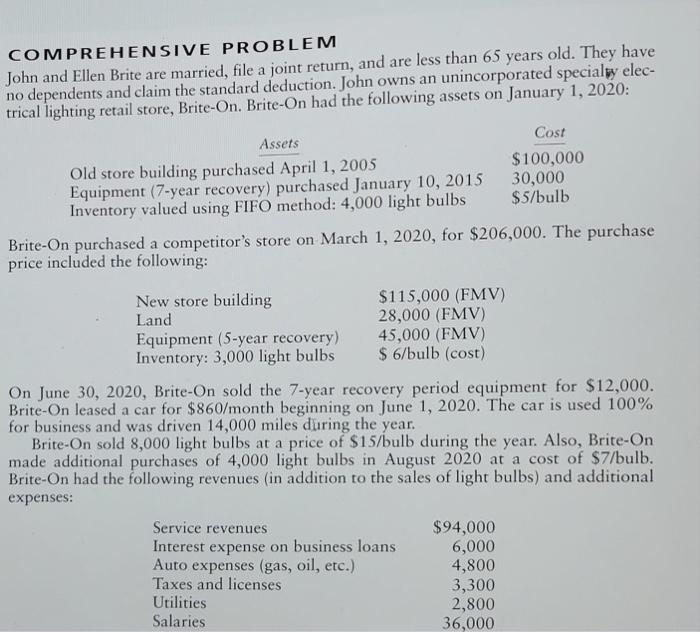

a COMPREHENSIVE PROBLEM John and Ellen Brite are married, file a joint return, and are less than 65 years old. They have no dependents and claim the standard deduction. John owns an unincorporated specialwy elec- trical lighting retail store, Brite-On. Brite-On had the following assets on January 1, 2020: Assets Cost Old store building purchased April 1, 2005 $100,000 Equipment (7-year recovery) purchased January 10, 2015 30,000 Inventory valued using FIFO method: 4,000 light bulbs $5/bulb Brite-On purchased a competitor's store on March 1, 2020, for $206,000. The purchase price included the following: New store building $115,000 (FMV) Land 28,000 (FMV) Equipment (5-year recovery) 45,000 (FMV) Inventory: 3,000 light bulbs $ 6/bulb (cost) On June 30, 2020, Brite-On sold the 7-year recovery period equipment for $12,000. Brite-On leased a car for $860/month beginning on June 1, 2020. The car is used 100% for business and was driven 14,000 miles during the year. Brite-On sold 8,000 light bulbs at a price of $15/bulb during the year. Also, Brite-On made additional purchases of 4,000 light bulbs in August 2020 at a cost of $7/bulb. Brite-On had the following revenues (in addition to the sales of light bulbs) and additional expenses: Service revenues Interest expense on business loans Auto expenses (gas, oil, etc.) Taxes and licenses Utilities Salaries $94,000 6,000 4,800 3,300 2,800 36,000

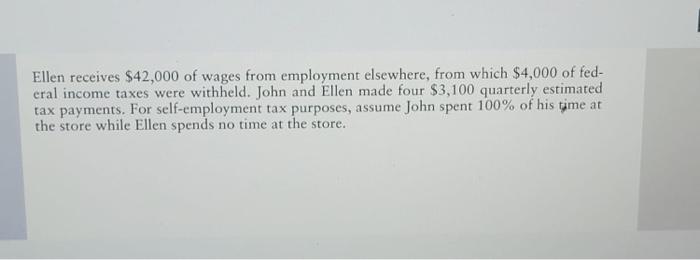

Ellen receives $42,000 of wages from employment elsewhere, from which $4,000 of fed- eral income taxes were withheld. John and Ellen made four $3,100 quarterly estimated tax payments. For self-employment tax purposes, assume John spent 100% of his time at the store while Ellen spends no time at the store.

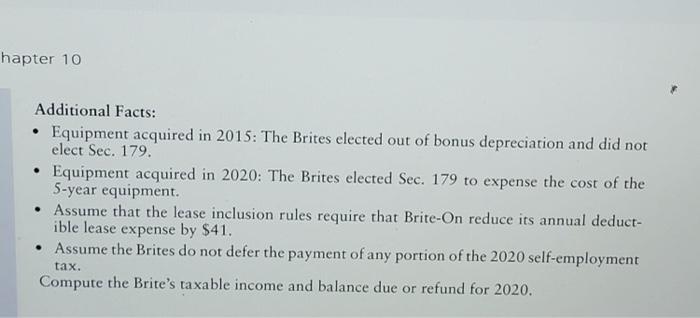

hapter 10 Additional Facts: • Equipment acquired in 2015: The Brites elected out of bonus depreciation and did not elect Sec. 179. Equipment acquired in 2020: The Brites elected Sec. 179 to expense the cost of the 5-year equipment. • Assume that the lease inclusion rules require that Brite-On reduce its annual deduct- ible lease expense by $41. • Assume the Brites do not defer the payment of any portion of the 2020 self-employment tax. Compute the Brite's taxable income and balance due or refund for 2020.