- Case 7 54 Cvp Analysis With Production And Marketing Decisions Taxes Appendix Lo 7 1 7 4 7 11 Oakley Company Manu 1 (101.43 KiB) Viewed 11 times

- Case 7 54 Cvp Analysis With Production And Marketing Decisions Taxes Appendix Lo 7 1 7 4 7 11 Oakley Company Manu 2 (61.8 KiB) Viewed 11 times

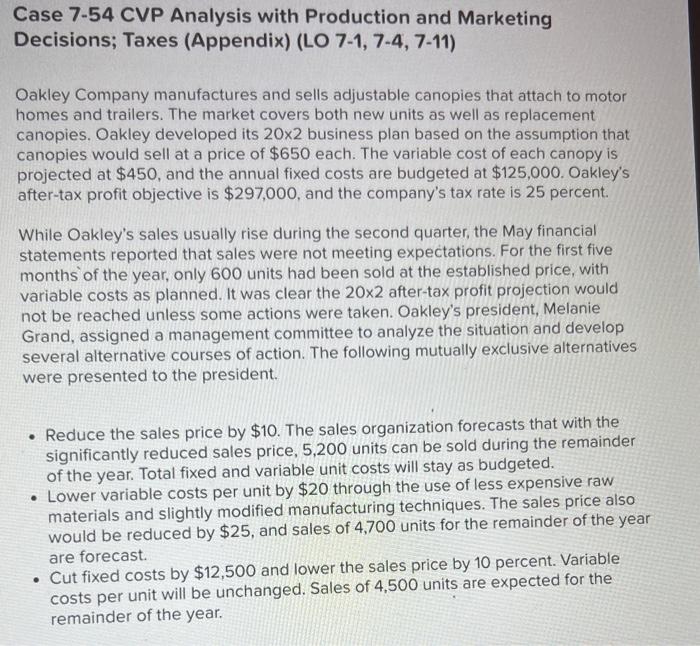

Case 7-54 CVP Analysis with Production and Marketing Decisions; Taxes (Appendix) (LO 7-1, 7-4, 7-11) Oakley

Company manufactures and sells adjustable canopies that attach to motor homes and trailers. The market covers both new units as well as replacement canopies. Oakley developed its 20x2 business plan based on the assumption that canopies would sell at a price of $650 each. The variable cost of each canopy is projected at $450, and the annual fixed costs are budgeted at $125,000. Oakley's after-tax profit objective is $297,000, and the

company's tax rate is 25 percent. While Oakley's sales usually rise during the second quarter, the May financial statements reported that sales were not meeting expectations. For the first five months of the year, only 600 units had been sold at the established price, with variable costs as planned. It was clear the 20x2 after-tax profit projection would not be reached unless some actions were taken. Oakley's president, Melanie Grand, assigned a management committee to analyze the situation and develop several alternative courses of action. The following mutually exclusive alternatives were presented to the president. • Reduce the sales price by $10. The sales organization forecasts that with the significantly reduced sales price, 5,200 units can be sold during the remainder of the year. Total fixed and variable unit costs will stay as budgeted. • Lower variable costs per unit by $20 through the use of less expensive raw materials and slightly modified manufacturing techniques. The sales price also would be reduced by $25, and sales of 4,700 units for the remainder of the year are forecast. • Cut fixed costs by $12,500 and lower the sales price by 10 percent. Variable costs per unit will be unchanged. Sales of 4,500 units are expected for the remainder of the year.

Required: 1. If no changes are made to the selling price or cost structure, determine the number of units that Oakley

Company must sell a. In order to break even. b. To achieve its after-tax profit objective. 2. Determine which one of the alternatives Oakley

Company should select to achieve its annual after-tax profit objective. Complete this

question by entering your answers in the tabs below. Required 1 Required 2 If no changes are made to the selling price or cost structure, determine the number of (Do not round intermediate calculcations and round your final answers up to the neares a. In order to break even. b. To achieve its after-tax profit objective. a. Number of units b. Number of units Pegunun 1 Required 2 >