Page 1 of 1

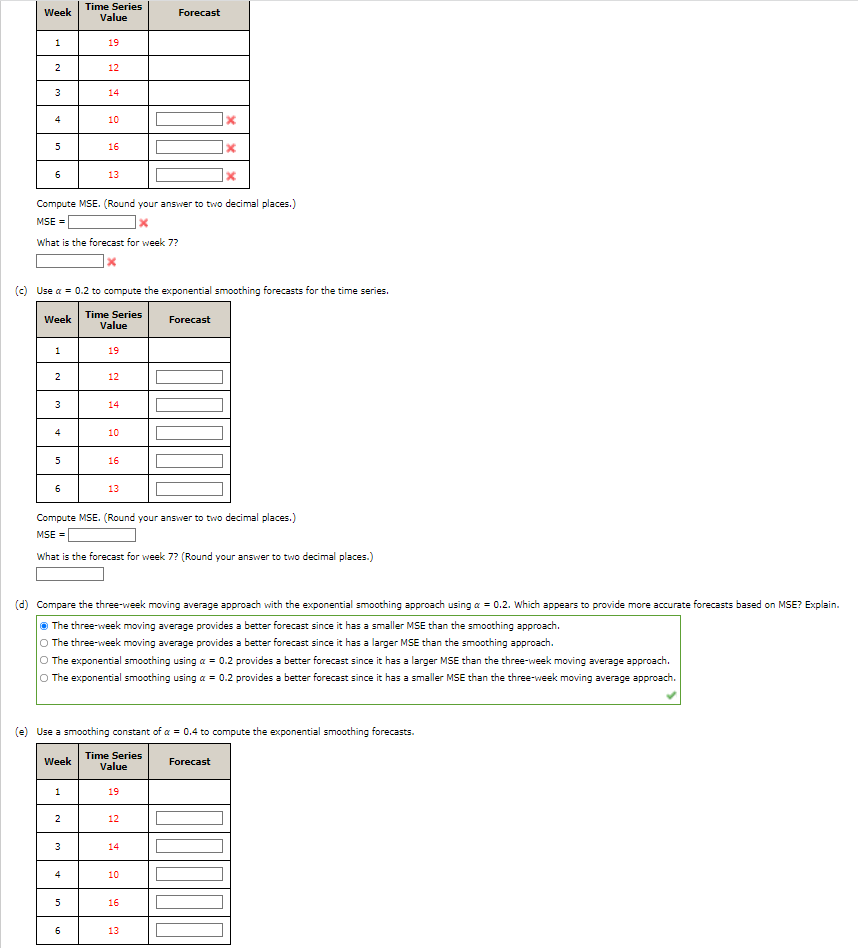

Week Time Series Value Forecast 1 19 N 12 3 14 4 10 U 16 6 13 Compute MSE. (Round your answer to two decimal places.) MS

Posted: Thu Apr 28, 2022 2:53 pm

by answerhappygod

- Week Time Series Value Forecast 1 19 N 12 3 14 4 10 U 16 6 13 Compute Mse Round Your Answer To Two Decimal Places Ms 1 (39.17 KiB) Viewed 22 times

Week Time Series Value Forecast 1 19 N 12 3 14 4 10 U 16 6 13 Compute MSE. (Round your answer to two decimal places.) MSE = What is the forecast for week 7? (2) Use a = 0.2 to compute the exponential smoothing forecasts for the time series. Week Time Series Value Forecast 1 19 2 12 3 14 4 10 5 16 6 13 Compute MSE. (Round your answer to two decimal places.) MSE = What is the forecast for week 7? (Round your answer to two decimal places.) (d) Compare the three-week moving average approach with the exponential smoothing approach using a = 0.2. Which appears to provide more accurate forecasts based on MSE? Explain. The three-week moving average provides a better forecast since it has a smaller MSE than the smoothing approach. O The three-week moving average provides a better forecast since it has a larger MSE than the smoothing approach. The exponential smoothing using a = 0.2 provides a better forecast since it has a larger MSE than the three-week moving average approach. O The exponential smoothing using a = 0.2 provides a better forecast since it has a smaller MSE than the three-week moving average approach. (e) Use a smoothing constant of a = 0.4 to compute the exponential smoothing forecasts. a Week Time Series Value Forecast 1 19 2 12 3 3 14 4 10 5 5 16 6 13