Page 1 of 1

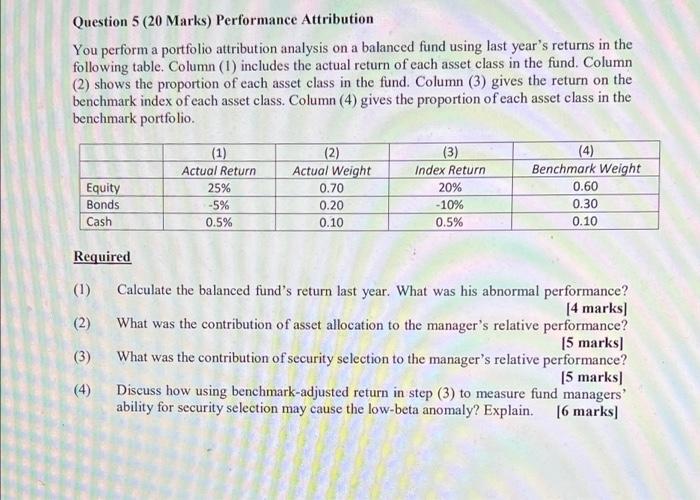

Question 5 (20 Marks) Performance Attribution You perform a portfolio attribution analysis on a balanced fund using last

Posted: Thu Apr 28, 2022 1:29 pm

by answerhappygod

- Question 5 20 Marks Performance Attribution You Perform A Portfolio Attribution Analysis On A Balanced Fund Using Last 1 (65.42 KiB) Viewed 24 times

Question 5 (20 Marks) Performance Attribution You perform a portfolio attribution analysis on a balanced fund using last year's returns in the following table Column (1) includes the actual return of each asset class in the fund. Column (2) shows the proportion of each asset class in the fund. Column (3) gives the return on the benchmark index of each asset class. Column (4) gives the proportion of each asset class in the benchmark portfolio (3) Equity Bonds Cash (1) Actual Return 25% -5% 0.5% (2) Actual Weight 0.70 0.20 0.10 Index Return 20% - 10% 0.5% (4) Benchmark Weight 0.60 0.30 0.10 (1) Required Calculate the balanced fund's return last year. What was his abnormal performance? [4 marks (2) What was the contribution of asset allocation to the manager's relative performance? 15 marks) (3) What was the contribution of security selection to the manager's relative performance? 15 marks) Discuss how using benchmark-adjusted return in step (3) to measure fund managers' ability for security selection may cause the low-beta anomaly? Explain. 16 marks (4)