Page 1 of 1

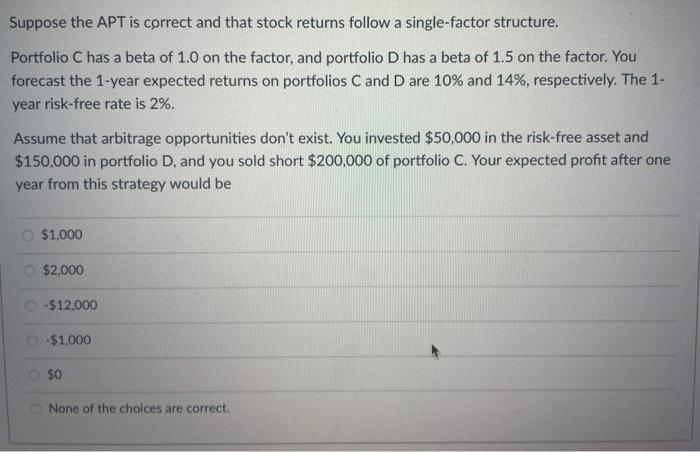

Suppose the APT is correct and that stock returns follow a single-factor structure. Portfolio C has a beta of 1.0 on the

Posted: Thu Apr 28, 2022 1:29 pm

by answerhappygod

- Suppose The Apt Is Correct And That Stock Returns Follow A Single Factor Structure Portfolio C Has A Beta Of 1 0 On The 1 (44.48 KiB) Viewed 19 times

Suppose the APT is correct and that stock returns follow a single-factor structure. Portfolio C has a beta of 1.0 on the factor, and portfolio D has a beta of 1.5 on the factor. You forecast the 1-year expected returns on portfolios C and D are 10% and 14%, respectively. The 1- year risk-free rate is 2%. Assume that arbitrage opportunities don't exist. You invested $50,000 in the risk-free asset and $150.000 in portfolio D, and you sold short $200,000 of portfolio C. Your expected profit after one year from this strategy would be $1,000 $2.000 -$12,000 -$1,000 $0 None of the choices are correct.