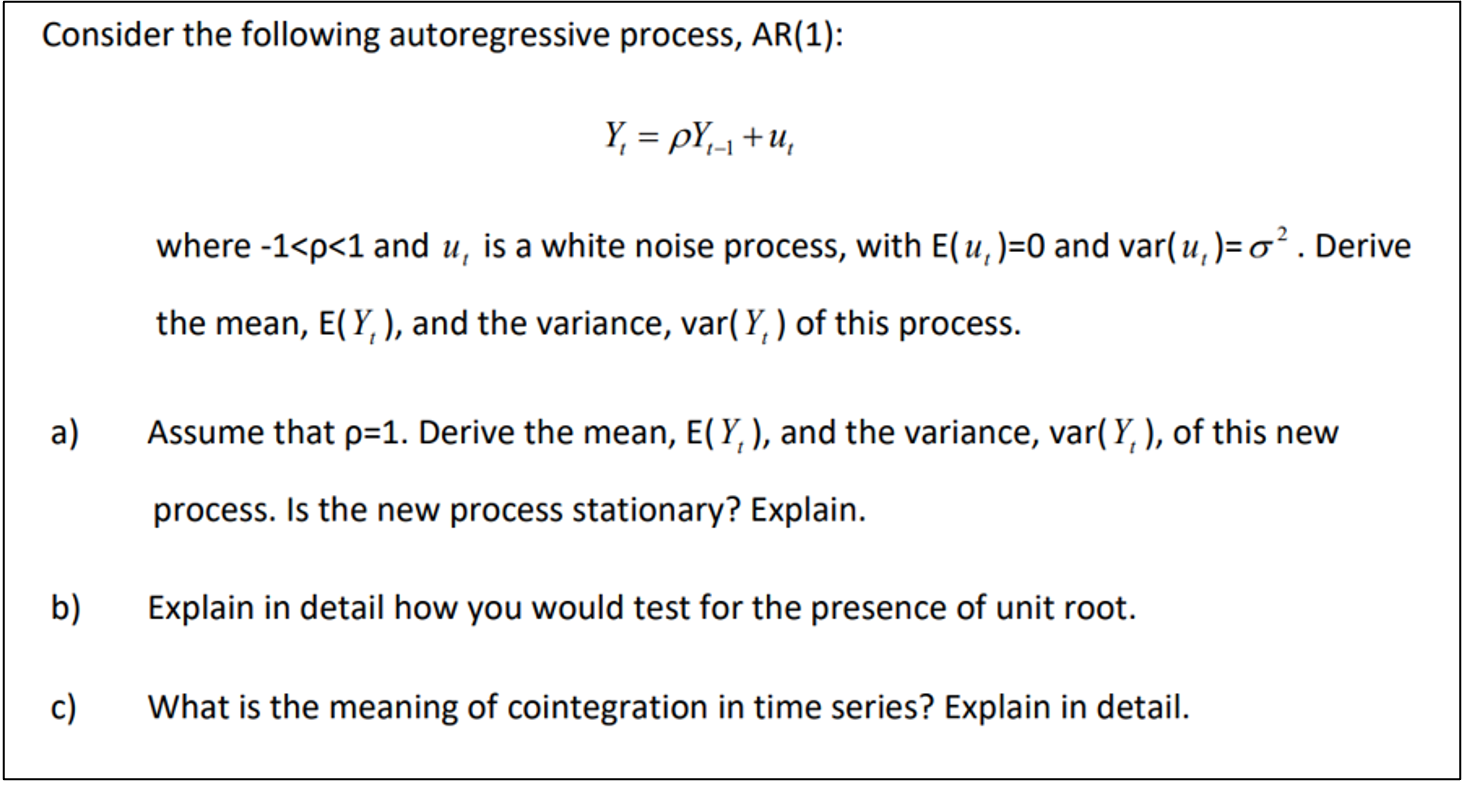

Consider the following autoregressive process, AR(1): Y = pY-+, where -1

Posted: Wed Apr 27, 2022 12:15 pm

- Consider The Following Autoregressive Process Ar 1 Y Py Where 1 P 1 And U Is A White Noise Process With E U 1 (344.67 KiB) Viewed 21 times

Consider the following autoregressive process, AR(1): Y = pY-+, where -1<p<1 and u, is a white noise process, with E(u,)=0 and var(u,)=0?. Derive the mean, E(Y,), and the variance, var(Y,) of this process. a) Assume that p=1. Derive the mean, E(Y,), and the variance, var(Y,), of this new process. Is the new process stationary? Explain. b) Explain in detail how you would test for the presence of unit root. c) What is the meaning of cointegration in time series? Explain in detail.

Posted: Wed Apr 27, 2022 12:15 pm

- Consider The Following Autoregressive Process Ar 1 Y Py Where 1 P 1 And U Is A White Noise Process With E U 1 (344.67 KiB) Viewed 21 times