Page 1 of 1

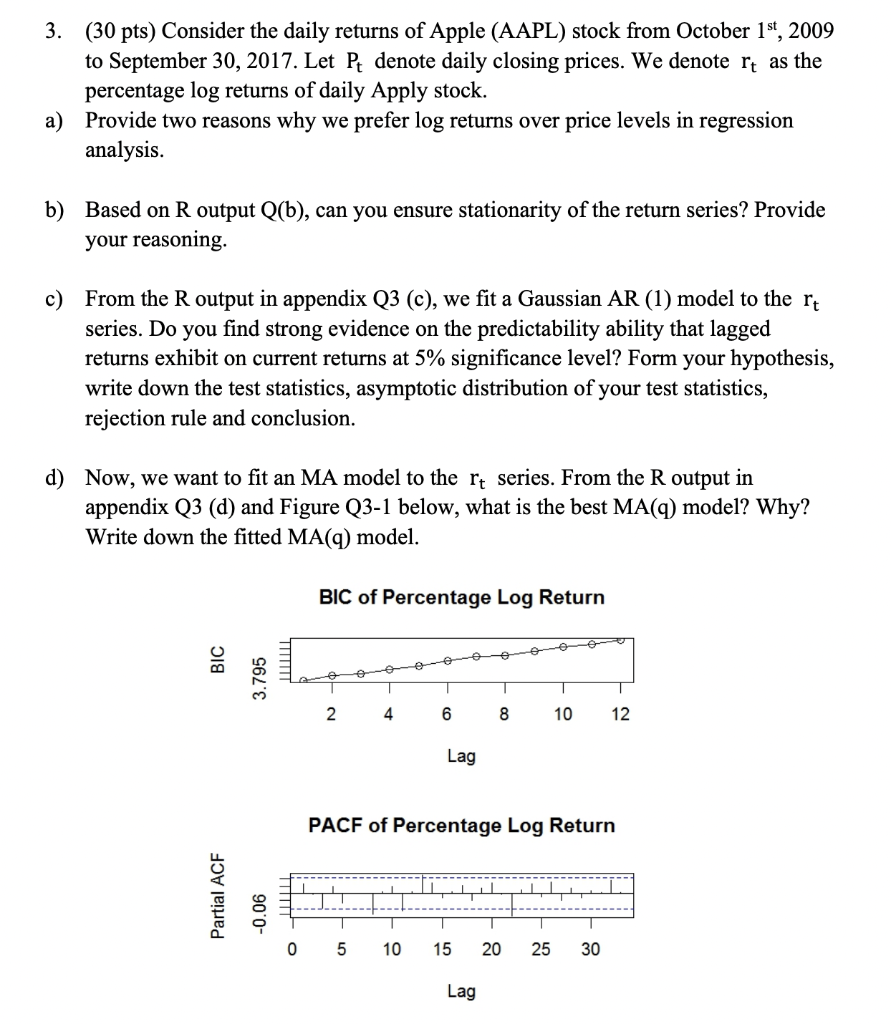

3. (30 pts) Consider the daily returns of Apple (AAPL) stock from October 1st, 2009 to September 30, 2017. Let Pt denote

Posted: Tue Apr 26, 2022 7:39 pm

by answerhappygod

- 3 30 Pts Consider The Daily Returns Of Apple Aapl Stock From October 1st 2009 To September 30 2017 Let Pt Denote 1 (444.3 KiB) Viewed 33 times

3. (30 pts) Consider the daily returns of Apple (AAPL) stock from October 1st, 2009 to September 30, 2017. Let Pt denote daily closing prices. We denote rt as the percentage log returns of daily Apply stock. a) Provide two reasons why we prefer log returns over price levels in regression analysis. b) Based on R output Q(b), can you ensure stationarity of the return series? Provide your reasoning c) From the R output in appendix Q3 (c), we fit a Gaussian AR (1) model to the rt series. Do you find strong evidence on the predictability ability that lagged returns exhibit on current returns at 5% significance level? Form your hypothesis, write down the test statistics, asymptotic distribution of your test statistics, rejection rule and conclusion. d) Now, we want to fit an MA model to the rt series. From the R output in appendix Q3 (d) and Figure Q3-1 below, what is the best MA(q) model? Why? Write down the fitted MA(q) model. BIC of Percentage Log Return BIC 3.795 1 2 4 6 8 10 12 Lag PACF of Percentage Log Return Partial ACF 90'0- i 0 5 10 15 20 25 30 Lag