Page 1 of 1

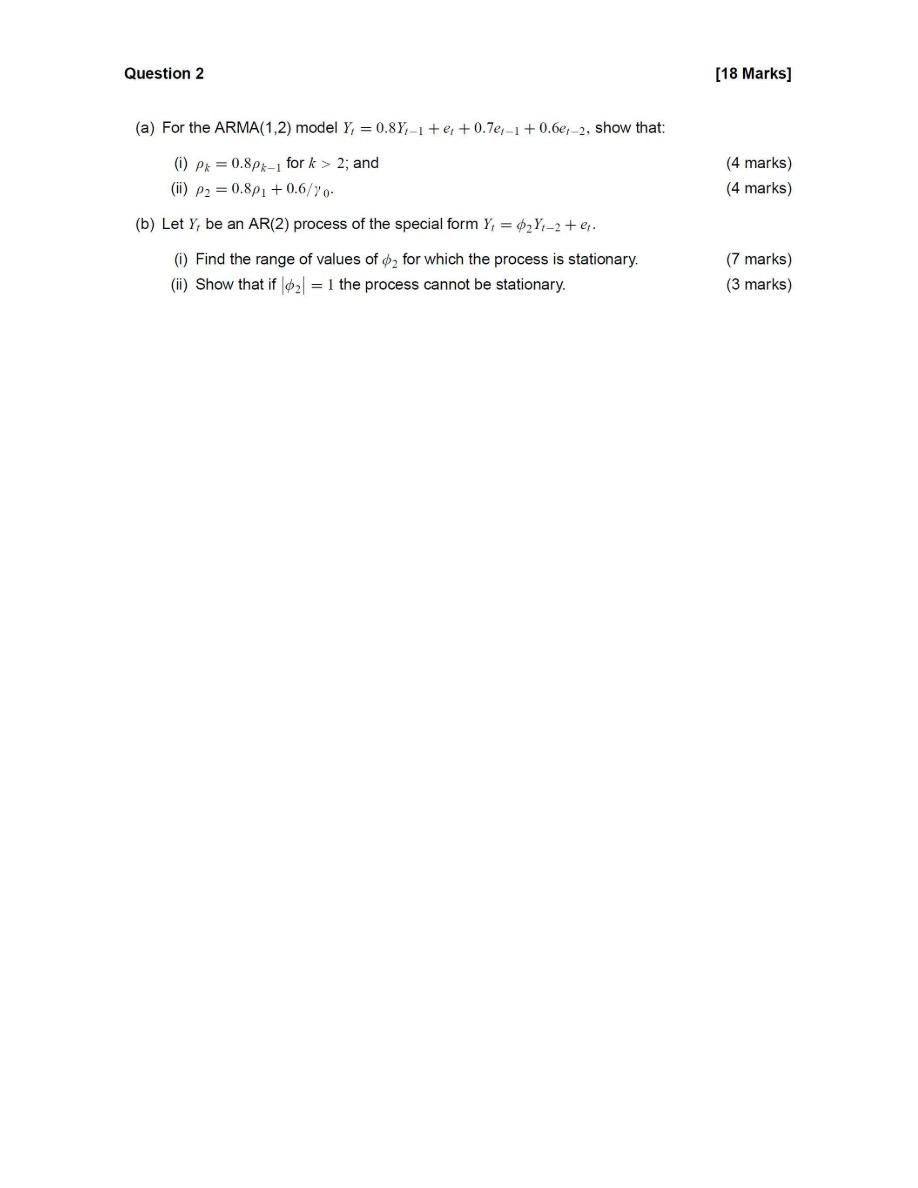

(a) For the ARMA(1,2) model Yt=0.8Yt−1+et+0.7et−1+0.6et−2, show that: (i) ρk=0.8ρk−1 for k>2; and (4 marks) (ii)

Posted: Thu Jul 14, 2022 4:53 pm

by answerhappygod

- 1 (36.9 KiB) Viewed 36 times

(a) For the ARMA(1,2) model Yt=0.8Yt−1+et+0.7et−1+0.6et−2, show that: (i) ρk=0.8ρk−1 for k>2; and (4 marks) (ii) ρ2=0.8ρ1+0.6/γ0. (4 marks) (b) Let Yt be an AR(2) process of the special form Yt=ϕ2Yt−2+et. (i) Find the range of values of ϕ2 for which the process is stationary. (7 marks) (ii) Show that if ∣ϕ2∣=1 the process cannot be stationary. (3 marks)