Page 1 of 1

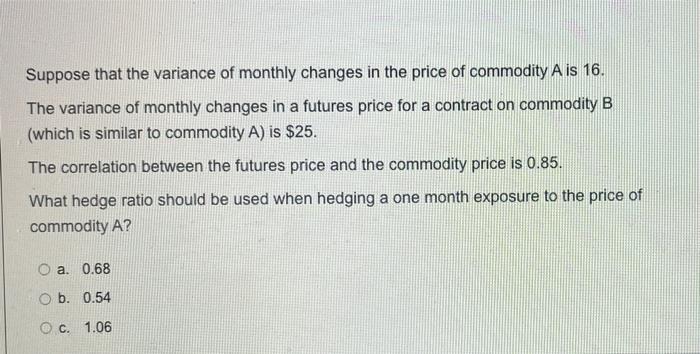

Suppose that the variance of monthly changes in the price of commodity A is 16. The variance of monthly changes in a fut

Posted: Tue Apr 26, 2022 11:13 am

by answerhappygod

- Suppose That The Variance Of Monthly Changes In The Price Of Commodity A Is 16 The Variance Of Monthly Changes In A Fut 1 (50.52 KiB) Viewed 54 times

Suppose that the variance of monthly changes in the price of commodity A is 16. The variance of monthly changes in a futures price for a contract on commodity B (which is similar to commodity A) is $25. The correlation between the futures price and the commodity price is 0.85. What hedge ratio should be used when hedging a one month exposure to the price of commodity A? O a. 0.68 O b. 0.54 OC. 1.06