Page 1 of 1

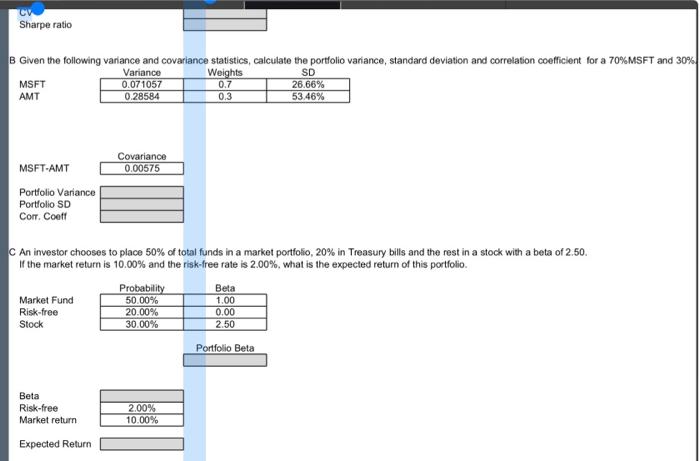

Sharpe ratio B Given the following variance and covariance statistics, calculate the portfolio variance, standard deviat

Posted: Tue Apr 26, 2022 11:08 am

by answerhappygod

- Sharpe Ratio B Given The Following Variance And Covariance Statistics Calculate The Portfolio Variance Standard Deviat 1 (30.47 KiB) Viewed 49 times

Sharpe ratio B Given the following variance and covariance statistics, calculate the portfolio variance, standard deviation and correlation coefficient for a 70%MSFT and 30% Variance Weights SD MSFT 0.071057 26,66% AMT 0.28584 53.46% 0.7 0,3 Covariance 0.00575 MSFT-AMT Portfolio Variance Portfolio SD Corr. Coeff C An investor chooses to place 50% of total funds in a market portfolio, 20% in Treasury bills and the rest in a stock with a beta of 2.50 If the market return is 10.00% and the risk-free rate is 2.00%, what is the expected return of this portfolio Probability 50.00% Risk-free 20.00% Stock Market Fund Beta 1.00 0.00 2.50 30.00% Portfolio Beta Beta Risk-free Market return 2.00% 10.00% Expected Return