Page 1 of 1

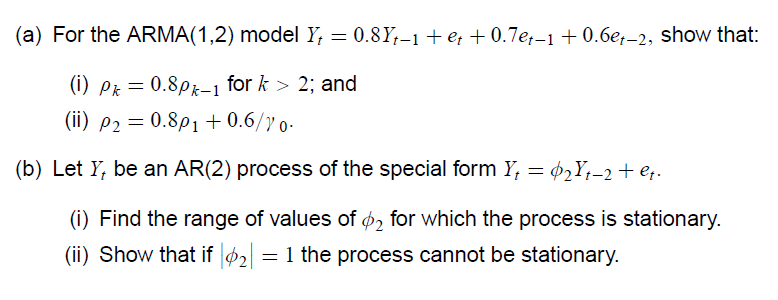

(a) For the ARMA(1,2) model Y₁ = 0.8Yt-1 + et +0.7et-1 +0.6e-2, show that: (i) Pk = 0.8pk-1 for k > 2; and (ii) P₂ = 0.8

Posted: Mon Jul 11, 2022 11:38 am

by answerhappygod

- A For The Arma 1 2 Model Y 0 8yt 1 Et 0 7et 1 0 6e 2 Show That I Pk 0 8pk 1 For K 2 And Ii P 0 8 1 (23.75 KiB) Viewed 34 times

(a) For the ARMA(1,2) model Y₁ = 0.8Yt-1 + et +0.7et-1 +0.6e-2, show that: (i) Pk = 0.8pk-1 for k > 2; and (ii) P₂ = 0.8p₁ +0.6/70- (b) Let Y, be an AR(2) process of the special form Y₁ = $2Y1–2 + €₁. (i) Find the range of values of 2 for which the process is stationary. (ii) Show that if |2| = 1 the process cannot be stationary.