Page 1 of 1

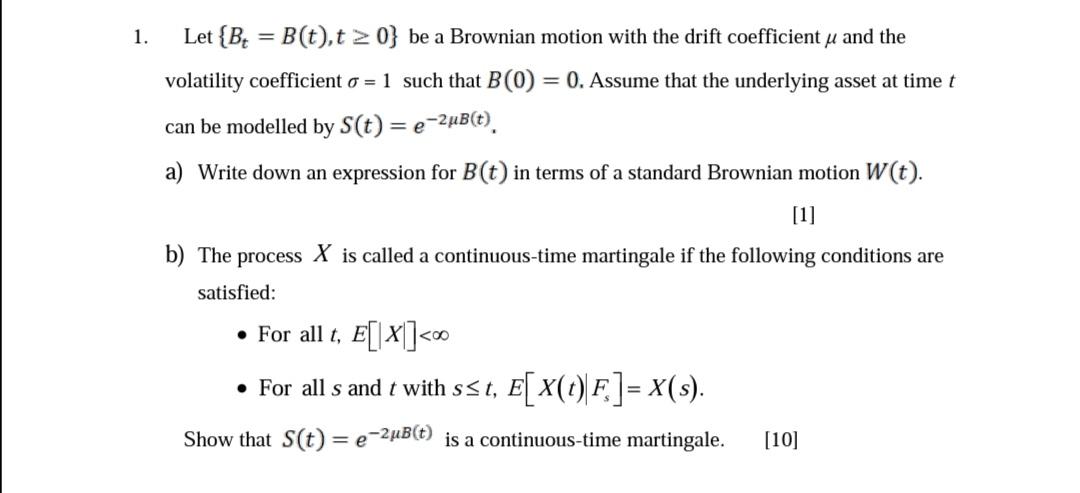

1. Let {B = B(t), t≥ 0} be a Brownian motion with the drift coefficient u and the volatility coefficient o = 1 such that

Posted: Sun Jul 10, 2022 10:10 am

by answerhappygod

- 1 Let B B T T 0 Be A Brownian Motion With The Drift Coefficient U And The Volatility Coefficient O 1 Such That 1 (44.05 KiB) Viewed 83 times

1. Let {B = B(t), t≥ 0} be a Brownian motion with the drift coefficient u and the volatility coefficient o = 1 such that B(0) = 0. Assume that the underlying asset at time t can be modelled by S(t) = e-2u(t) е a) Write down an expression for B (t) in terms of a standard Brownian motion W(t). [1] b) The process X is called a continuous-time martingale if the following conditions are satisfied: • For all t, E[X]<∞ • For all s and t with s≤t, E[X(t) F] = X(s). is a continuous-time martingale. Show that S(t)=e-2μB(t) [10]