Page 1 of 1

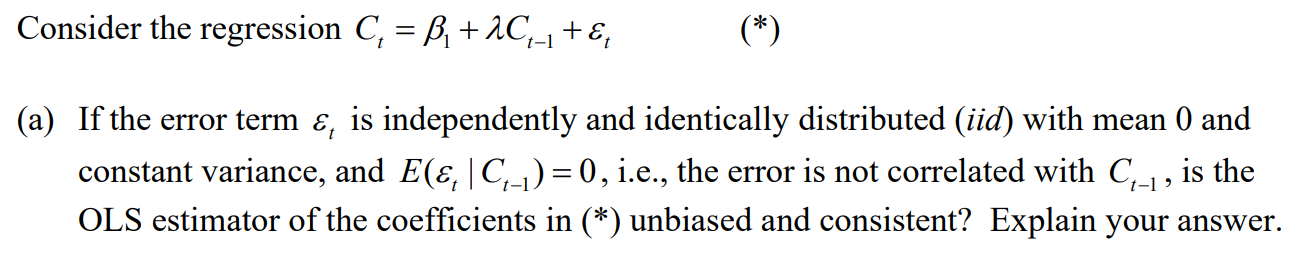

Consider the regression C, = B. +2C–+, (*) t- (a) If the error term ε, is independently and identically distributed (iid

Posted: Mon Apr 18, 2022 9:21 am

by answerhappygod

- 1 (74.61 KiB) Viewed 31 times

Consider the regression C, = B. +2C–+, (*) t- (a) If the error term ε, is independently and identically distributed (iid) with mean 0 and constant variance, and E(Ę,C-1) = 0, i.e., the error is not correlated with C-1, is the OLS estimator of the coefficients in (*) unbiased and consistent? Explain your answer. 't-