Page 1 of 1

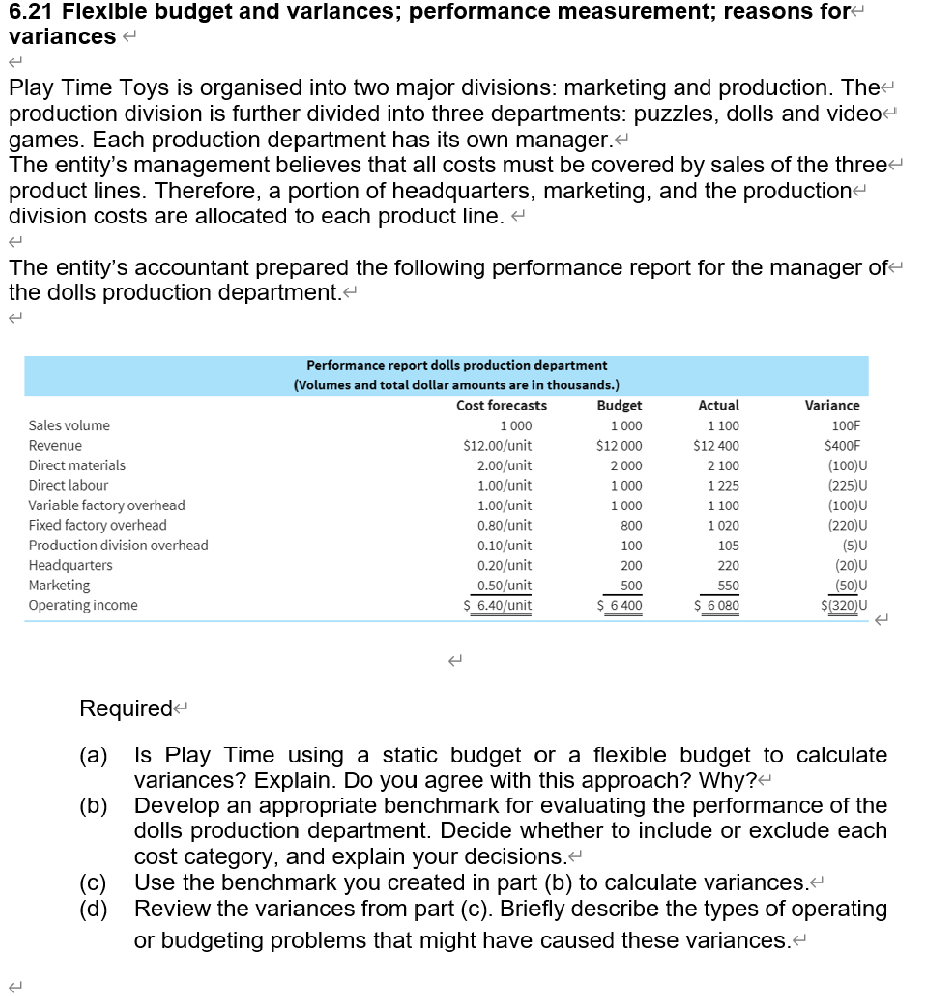

6.21 Flexible budget and varlances; performance measurement; reasons for- variances Play Time Toys is organised into two

Posted: Sun Apr 17, 2022 7:07 pm

by answerhappygod

- 6 21 Flexible Budget And Varlances Performance Measurement Reasons For Variances Play Time Toys Is Organised Into Two 1 (139.89 KiB) Viewed 33 times

6.21 Flexible budget and varlances; performance measurement; reasons for- variances Play Time Toys is organised into two major divisions: marketing and production. The production division is further divided into three departments: puzzles, dolls and videos games. Each production department has its own manager. The entity's management believes that all costs must be covered by sales of the three- product lines. Therefore, a portion of headquarters, marketing, and the production division costs are allocated to each product line. 4 The entity's accountant prepared the following performance report for the manager of the dolls production department. Sales volume Revenue Direct materials Direct labour Variable factory overhead Fixed factory overhead Production division overhead Headquarters Marketing Operating income Performance report dolls production department (Volumes and total dollar amounts are in thousands.) Cost forecasts Budget 1 000 1 000 $12.00/unit $12000 2.00/unit 2000 1.00/unit 1000 1.00/unit 1 000 0.80/unit 800 0.10/unit 100 0.20 unit 200 0.50/unit 500 $ 6.40/unit $ 6400 Actual 1 100 $12 400 2 100 1 225 1 100 1020 105 220 550 $ 5080 Variance 100F $400F (100) (225) (100) (220) (5)U (20) (50)U $(320)U Required (a) Is Play Time using a static budget or a flexible budget to calculate variances? Explain. Do you agree with this approach? Why? (b) Develop an appropriate benchmark for evaluating the performance of the dolls production department. Decide whether to include or exclude each cost category, and explain your decisions. (c) Use the benchmark you created in part (b) to calculate variances. (d) Review the variances from part (c). Briefly describe the types of operating or budgeting problems that might have caused these variances.