Page 1 of 1

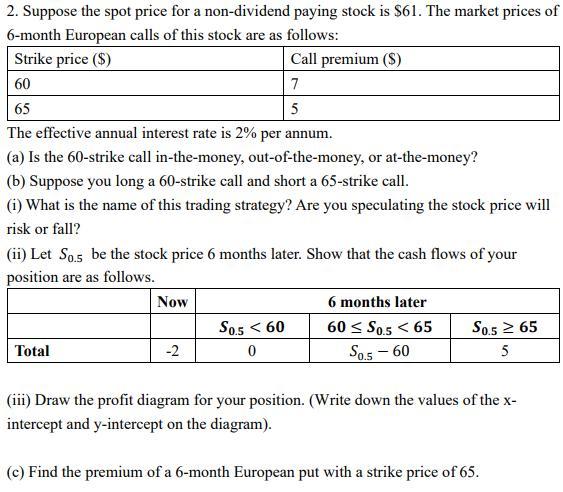

2. Suppose the spot price for a non-dividend paying stock is $61. The market prices of 6-month European calls of this st

Posted: Sun Apr 17, 2022 6:28 pm

by answerhappygod

- 2 Suppose The Spot Price For A Non Dividend Paying Stock Is 61 The Market Prices Of 6 Month European Calls Of This St 1 (57.11 KiB) Viewed 34 times

2. Suppose the spot price for a non-dividend paying stock is $61. The market prices of 6-month European calls of this stock are as follows: Strike price ($) Call premium ($) 60 7 65 5 The effective annual interest rate is 2% per annum. (a) Is the 60-strike call in-the-money, out-of-the-money, or at-the-money? (b) Suppose you long a 60-strike call and short a 65-strike call. (1) What is the name of this trading strategy? Are you speculating the stock price will risk or fall? (ii) Let So.5 be the stock price 6 months later. Show that the cash flows of your position are as follows. Now 6 months later Sos < 60 60 < 50.5 < 65 S0.5 > 65 Total -2 0 Sos -60 5 0 (iii) Draw the profit diagram for your position. (Write down the values of the x- intercept and y-intercept on the diagram). (c) Find the premium of a 6-month European put with a strike price of 65. a