Page 1 of 1

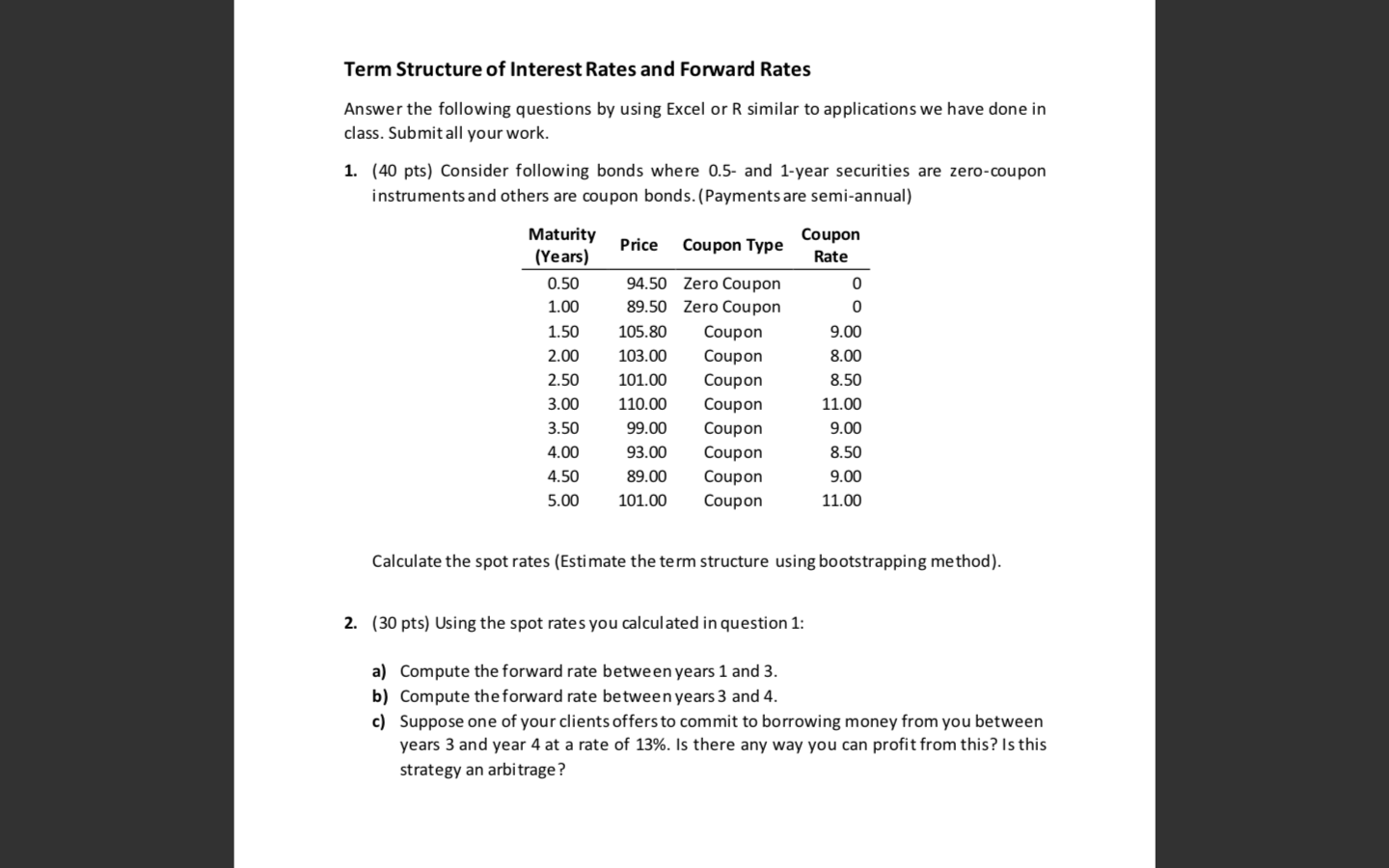

Term Structure of Interest Rates and Forward Rates Answer the following questions by using Excel or R similar to applica

Posted: Sun Apr 17, 2022 6:21 pm

by answerhappygod

- Term Structure Of Interest Rates And Forward Rates Answer The Following Questions By Using Excel Or R Similar To Applica 1 (115.54 KiB) Viewed 51 times

Term Structure of Interest Rates and Forward Rates Answer the following questions by using Excel or R similar to applications we have done in class. Submit all your work. 1. (40 pts) Consider following bonds where 0.5- and 1-year securities are zero-coupon instruments and others are coupon bonds. (Payments are semi-annual) Price Coupon Type Coupon Rate Maturity (Years) 0.50 1.00 1.50 2.00 2.50 3.00 3.50 4.00 4.50 5.00 94.50 Zero Coupon 89.50 Zero Coupon 105.80 Coupon 103.00 Coupon 101.00 Coupon 110.00 Coupon 99.00 Coupon 93.00 Coupon 89.00 Coupon 101.00 Coupon 0 0 9.00 8.00 8.50 11.00 9.00 8.50 9.00 11.00 Calculate the spot rates (Estimate the term structure using bootstrapping method). 2. (30 pts) Using the spot rates you calculated in question 1: a) Compute the forward rate between years 1 and 3. b) Compute the forward rate between years 3 and 4. c) Suppose one of your clients offers to commit to borrowing money from you between years 3 and year 4 at a rate of 13%. Is there any way you can profit from this? Is this strategy an arbitrage ?