Page 1 of 1

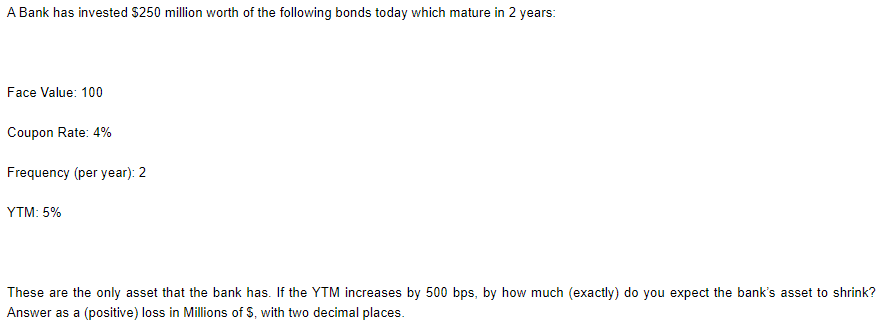

A Bank has invested $250 million worth of the following bonds today which mature in 2 years: Face Value: 100 Coupon Rate

Posted: Sun Apr 17, 2022 6:18 pm

by answerhappygod

- A Bank Has Invested 250 Million Worth Of The Following Bonds Today Which Mature In 2 Years Face Value 100 Coupon Rate 1 (12.02 KiB) Viewed 40 times

A Bank has invested $250 million worth of the following bonds today which mature in 2 years: Face Value: 100 Coupon Rate: 4% Frequency (per year): 2 YTM: 5% These are the only asset that the bank has. If the YTM increases by 500 bps, by how much (exactly) do you expect the bank's asset to shrink? Answer as a (positive) loss in Millions of S, with two decimal places.