Page 1 of 1

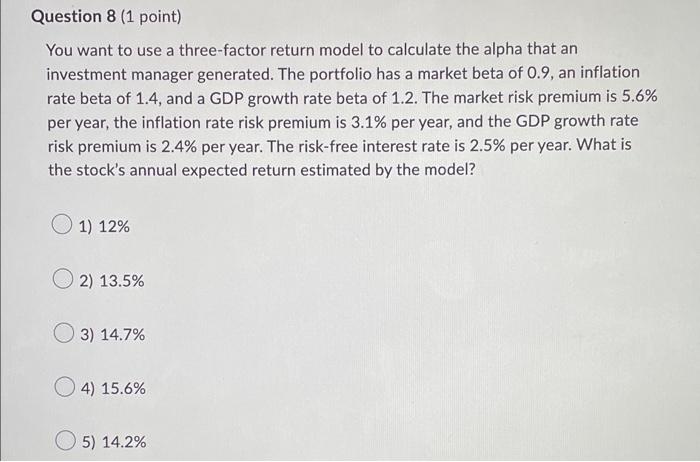

Question 8 (1 point) You want to use a three-factor return model to calculate the alpha that an investment manager gener

Posted: Wed Jul 06, 2022 6:45 pm

by answerhappygod

- Question 8 1 Point You Want To Use A Three Factor Return Model To Calculate The Alpha That An Investment Manager Gener 1 (37.75 KiB) Viewed 22 times

Question 8 (1 point) You want to use a three-factor return model to calculate the alpha that an investment manager generated. The portfolio has a market beta of 0.9, an inflation rate beta of 1.4, and a GDP growth rate beta of 1.2. The market risk premium is 5.6% per year, the inflation rate risk premium is 3.1% per year, and the GDP growth rate risk premium is 2.4% per year. The risk-free interest rate is 2.5% per year. What is the stock's annual expected return estimated by the model? 1) 12% 2) 13.5% 3) 14.7% 4) 15.6% 5) 14.2%