Page 1 of 1

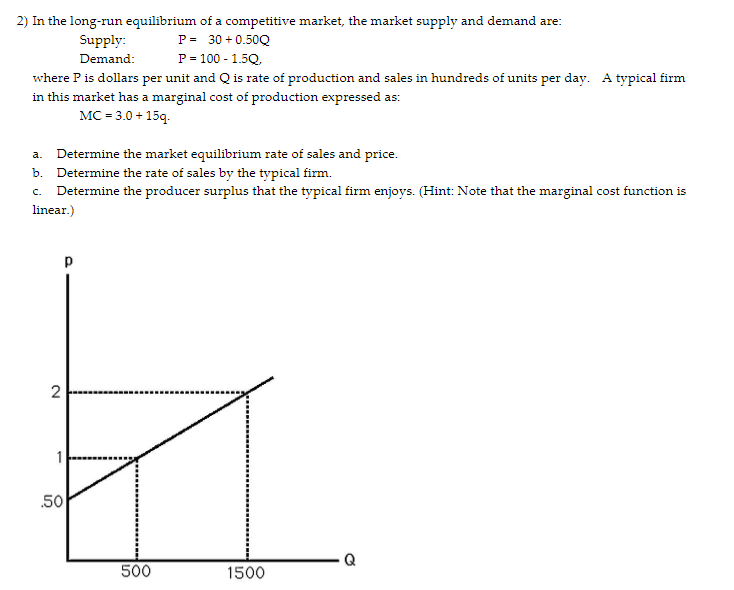

2) In the long-run equilibrium of a competitive market, the market supply and demand are: Supply: P = 30 +0.50Q Demand:

Posted: Wed Jul 06, 2022 6:22 pm

by answerhappygod

- 2 In The Long Run Equilibrium Of A Competitive Market The Market Supply And Demand Are Supply P 30 0 50q Demand 1 (35.67 KiB) Viewed 17 times

2) In the long-run equilibrium of a competitive market, the market supply and demand are: Supply: P = 30 +0.50Q Demand: P = 100-1.5Q, where P is dollars per unit and Q is rate of production and sales in hundreds of units per day. A typical firm in this market has a marginal cost of production expressed as: MC = 3.0+ 15q. a. Determine the market equilibrium rate of sales and price. b. Determine the rate of sales by the typical firm. C. Determine the producer surplus that the typical firm enjoys. (Hint: Note that the marginal cost function is linear.) 2 .50 500 1500