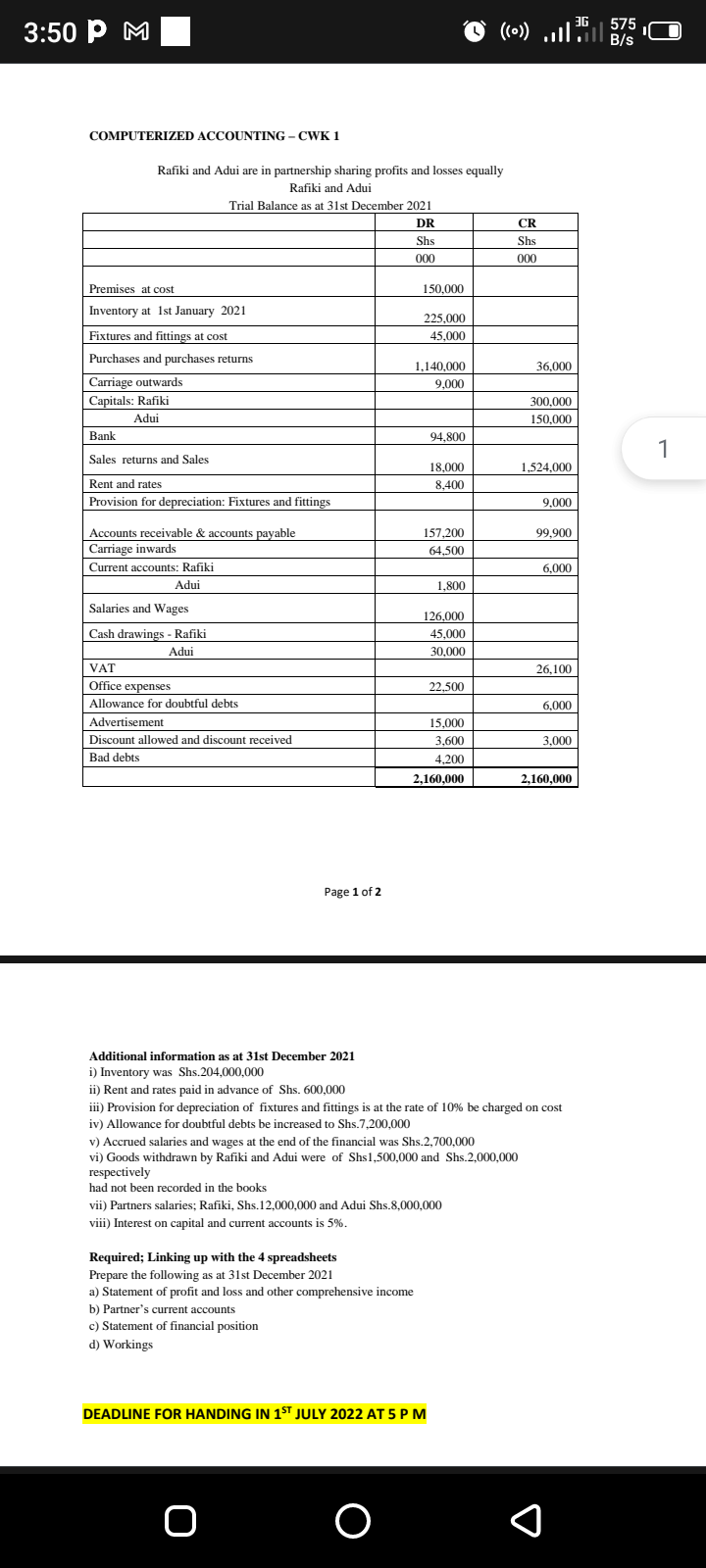

- 3 50 Pm Computerized Accounting Cwk 1 Rafiki And Adui Are In Partnership Sharing Profits And Losses Equally Rafiki And 1 (144.89 KiB) Viewed 19 times

3:50 PM COMPUTERIZED ACCOUNTING - CWK 1 Rafiki and Adui are in partnership sharing profits and losses equally Rafiki and Adui Trial Balance as at 31st December 2021 Premises at cost Inventory at 1st January 2021 Fixtures and fittings at cost Purchases and purchases returns Carriage outwards Capitals: Rafiki Adui Bank Sales returns and Sales Rent and rates Provision for depreciation: Fixtures and fittings Accounts receivable & accounts payable Carriage inwards Current accounts: Rafiki Adui Salaries and Wages Cash drawings - Rafiki Adui VAT Office expenses Allowance for doubtful debts Advertisement Discount allowed and discount received Bad debts Page 1 of 2 Additional information as at 31st December 2021 i) Inventory was Shs.204,000,000 DR Shs 000 O 150.000 Required; Linking up with the 4 spreadsheets Prepare the following as at 31st December 2021 a)

Statement of profit and loss and other comprehensive income b) Partner's current accounts c)

Statement of financial position d) Workings • (۰) || 75 B/s O 225,000 45,000 1,140,000 9,000 94,800 18,000 8,400 157,200 64,500 DEADLINE FOR HANDING IN 1ST JULY 2022 AT 5 P M 1,800 126,000 45,000 30,000 15,000 3,600 4,200 2,160,000 22,500 v) Accrued salaries and wages at the end of the financial was Shs.2,700,000 vi) Goods withdrawn by Rafiki and Adui were of Shs1,500,000 and Shs.2,000,000 respectively had not been recorded in the books vii) Partners salaries; Rafiki, Shs.12,000,000 and Adui Shs.8,000,000 viii) Interest on capital and current accounts is 5%. CR Shs 000 36,000 300,000 150,000 1,524,000 9,000 99,900 6,000 ii) Rent and rates paid in advance of Shs. 600,000 iii) Provision for depreciation of fixtures and fittings is at the rate of 10% be charged on cost iv) Allowance for doubtful debts be increased to Shs.7,200,000 26,100 6,000 3,000 2,160,000 ← 1