Page 1 of 1

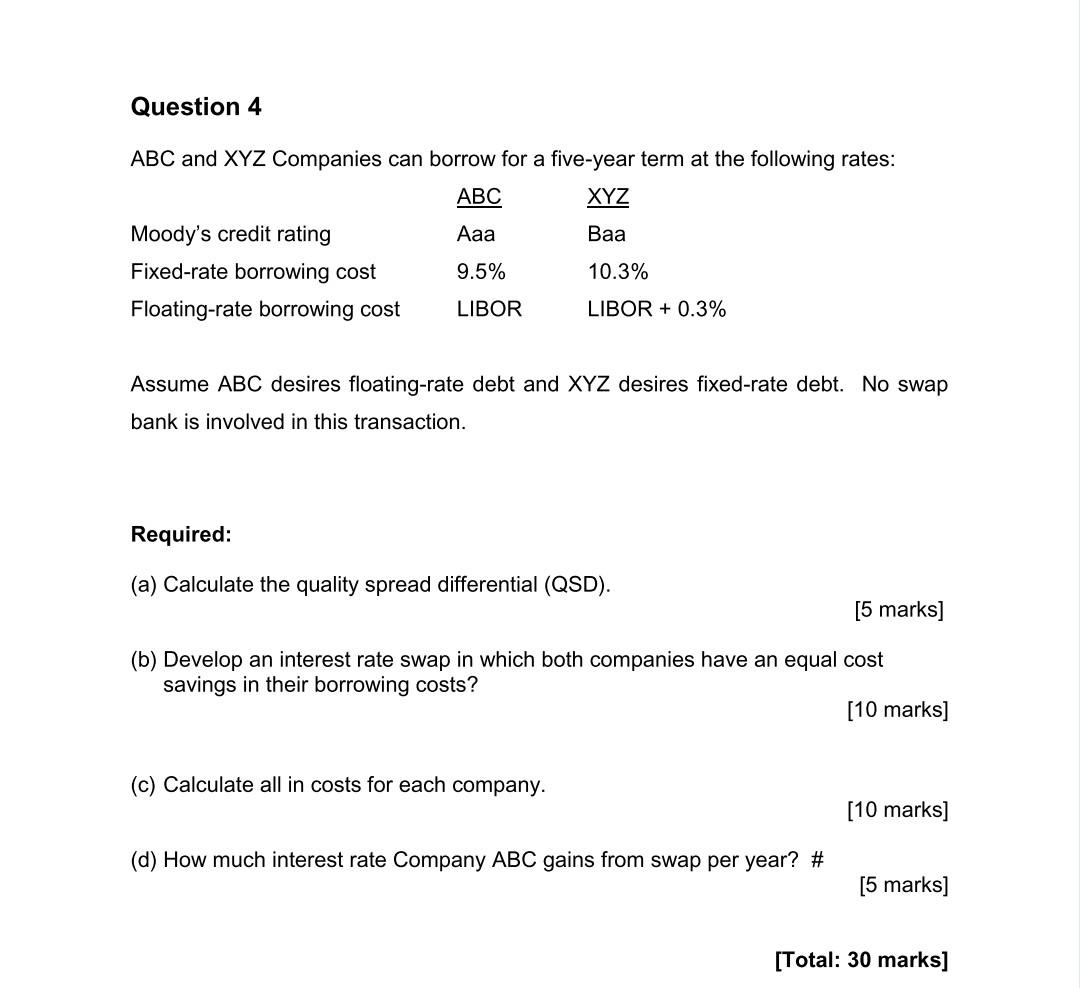

Question 4 ABC and XYZ Companies can borrow for a five-year term at the following rates: ABC XYZ Aaa Baa 9.5% 10.3% LIBO

Posted: Sun Jul 03, 2022 4:16 pm

by answerhappygod

- Question 4 Abc And Xyz Companies Can Borrow For A Five Year Term At The Following Rates Abc Xyz Aaa Baa 9 5 10 3 Libo 1 (77.96 KiB) Viewed 9 times

Question 4 ABC and XYZ Companies can borrow for a five-year term at the following rates: ABC XYZ Aaa Baa 9.5% 10.3% LIBOR LIBOR + 0.3% Moody's credit rating Fixed-rate borrowing cost Floating-rate borrowing cost Assume ABC desires floating-rate debt and XYZ desires fixed-rate debt. No swap bank is involved in this transaction. Required: (a) Calculate the quality spread differential (QSD). [5 marks] (b) Develop an interest rate swap in which both companies have an equal cost savings in their borrowing costs? [10 marks] (c) Calculate all in costs for each

company. (d) How much interest rate

Company ABC gains from swap per year? # [10 marks] [5 marks] [Total: 30 marks]