Page 1 of 1

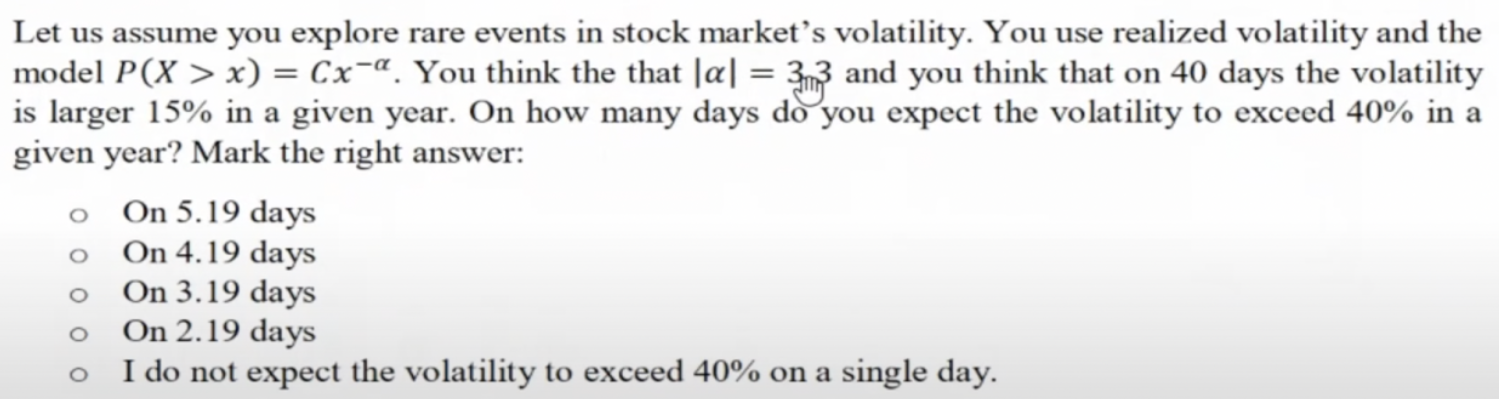

Let us assume you explore rare events in stock market’s volatility. You use realized volatility and the model P(X > x) =

Posted: Wed Apr 06, 2022 9:09 am

by answerhappygod

- Let Us Assume You Explore Rare Events In Stock Market S Volatility You Use Realized Volatility And The Model P X X 1 (628.13 KiB) Viewed 47 times

Let us assume you explore rare events in stock market’s volatility. You use realized volatility and the model P(X > x) = Cx-a. You think the that |a| = 33 and you think that on 40 days the volatility is larger 15% in a given year. On how many days do you expect the volatility to exceed 40% in a given year? Mark the right answer: o On 5.19 days On 4.19 days On 3.19 days On 2.19 days I do not expect the volatility to exceed 40% on a single day.