Page 1 of 1

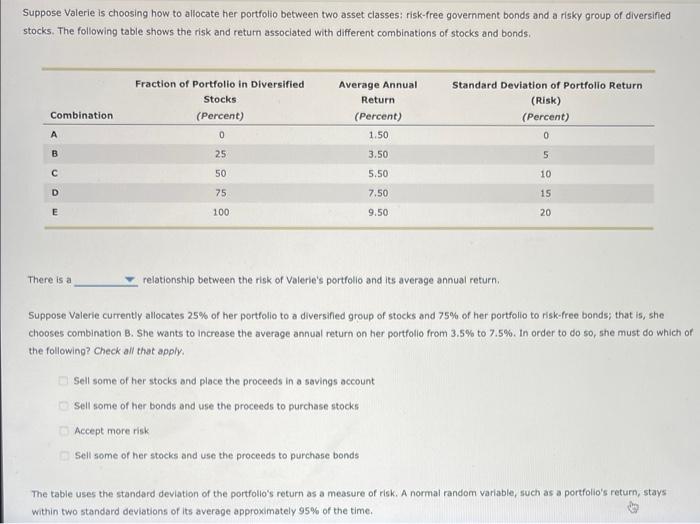

Suppose Valerie is choosing how to allocate her portfolio between two asset classes: risk-free government bonds and a ri

Posted: Sun Jul 03, 2022 1:02 pm

by answerhappygod

- Suppose Valerie Is Choosing How To Allocate Her Portfolio Between Two Asset Classes Risk Free Government Bonds And A Ri 1 (42.19 KiB) Viewed 13 times

- Suppose Valerie Is Choosing How To Allocate Her Portfolio Between Two Asset Classes Risk Free Government Bonds And A Ri 2 (7.96 KiB) Viewed 13 times

Suppose Valerie is choosing how to allocate her portfolio between two asset classes: risk-free government bonds and a risky group of diversified stocks. The following table shows the risk and return associated with different combinations of stocks and bonds. Combination A B с D There is a Fraction of Portfolio in Diversified Stocks (Percent) 0 25 50 75 100 Average Annual Return (Percent) 1.50 3.50 5.50 7.50 9.50 Standard Deviation of Portfolio Return (Risk) (Percent) 0 relationship between the risk of Valerie's portfolio and its average annual return. Sell some of her stocks and place the proceeds in a savings account Sell some of her bonds and use the proceeds to purchase stocks Accept more risk Sell some of her stocks and use the proceeds to purchase bonds 5 10 15 20 Suppose Valerie currently allocates 25% of her portfolio to a diversified group of stocks and 75% of her portfolio to risk-free bonds; that is, she chooses combination B. She wants to increase the average annual return on her portfolio from 3.5% to 7.5%. In order to do so, she must do which of the following? Check all that apply. The table uses the standard deviation of the portfolio's return as a measure of risk. A normal random variable, such as a portfolio's return, stays within two standard deviations of its average approximately 95% of the time.

Suppose Valerie modifies her portfolio to contain 50% diversified stocks and 50% risk-free government bonds; that is, she chooses combination C. The average annual return for this type of portfolio is 5.5%, but given the standard deviation of 10%, the returns will typically (about 95% of the time) vary from a gain of to a loss of