Page 1 of 1

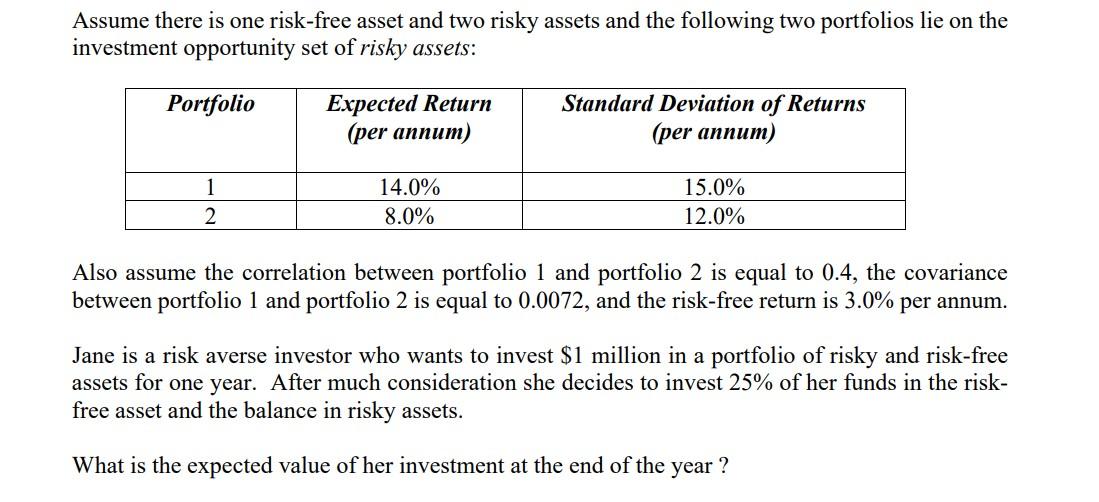

Assume there is one risk-free asset and two risky assets and the following two portfolios lie on the investment opportun

Posted: Sun Jul 03, 2022 6:49 am

by answerhappygod

- Assume There Is One Risk Free Asset And Two Risky Assets And The Following Two Portfolios Lie On The Investment Opportun 1 (80.48 KiB) Viewed 11 times

Assume there is one risk-free asset and two risky assets and the following two portfolios lie on the investment opportunity set of risky assets: Portfolio 1 2 Expected Return (per annum) 14.0% 8.0% Standard Deviation of Returns (per annum) 15.0% 12.0% Also assume the correlation between portfolio 1 and portfolio 2 is equal to 0.4, the covariance between portfolio 1 and portfolio 2 is equal to 0.0072, and the risk-free return is 3.0% per annum. Jane is a risk averse investor who wants to invest $1 million in a portfolio of risky and risk-free assets for one year. After much consideration she decides to invest 25% of her funds in the risk- free asset and the balance in risky assets. What is the expected value of her investment at the end of the year ?