Page 1 of 1

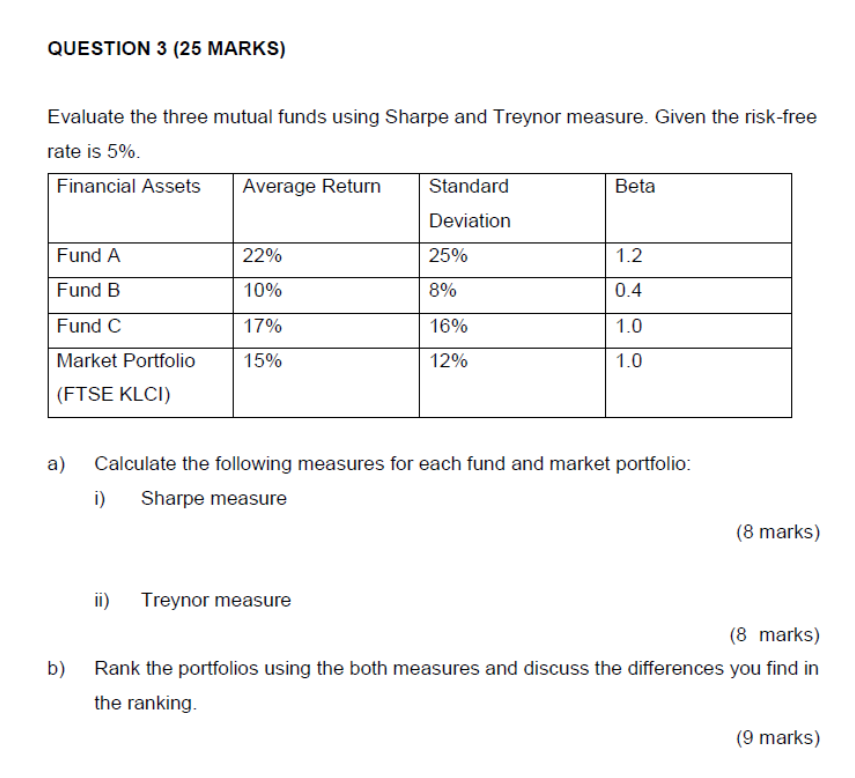

QUESTION 3 (25 MARKS) Evaluate the three mutual funds using Sharpe and Treynor measure. Given the risk-free rate is 5%.

Posted: Sun Jul 03, 2022 6:43 am

by answerhappygod

- Question 3 25 Marks Evaluate The Three Mutual Funds Using Sharpe And Treynor Measure Given The Risk Free Rate Is 5 1 (116.48 KiB) Viewed 30 times

QUESTION 3 (25 MARKS) Evaluate the three mutual funds using Sharpe and Treynor measure. Given the risk-free rate is 5%. Financial Assets Fund A Fund B Fund C Market Portfolio (FTSE KLCI) a) b) Average Return 22% 10% 17% 15% Standard Deviation ii) Treynor measure 25% 8% 16% 12% Beta 1.2 0.4 1.0 1.0 Calculate the following measures for each fund and market portfolio: i) Sharpe measure (8 marks) (8 marks) Rank the portfolios using the both measures and discuss the differences you find in the ranking. (9 marks)