Page 1 of 1

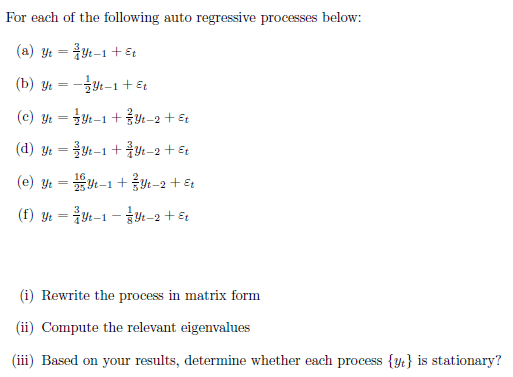

For each of the following auto regressive processes below: (a) Yt=Yt-1 + Et (b) ytt-1 + Et = (c) Yt=Yt-1+Y₁-2 1-2 + Et (

Posted: Fri Jul 01, 2022 8:14 am

by answerhappygod

- For Each Of The Following Auto Regressive Processes Below A Yt Yt 1 Et B Ytt 1 Et C Yt Yt 1 Y 2 1 2 Et 1 (25.85 KiB) Viewed 32 times

For each of the following auto regressive processes below: (a) Yt=Yt-1 + Et (b) ytt-1 + Et = (c) Yt=Yt-1+Y₁-2 1-2 + Et (d) Yt=Yt-1+Yt-2 + Et (e) Yt=Yt-1+Yt−2+ Et (f) Yt Yt-1 - Yt-2 + Et = (i) Rewrite the process in matrix form (ii) Compute the relevant eigenvalues (iii) Based on your results, determine whether each process {y} is stationary?