Page 1 of 1

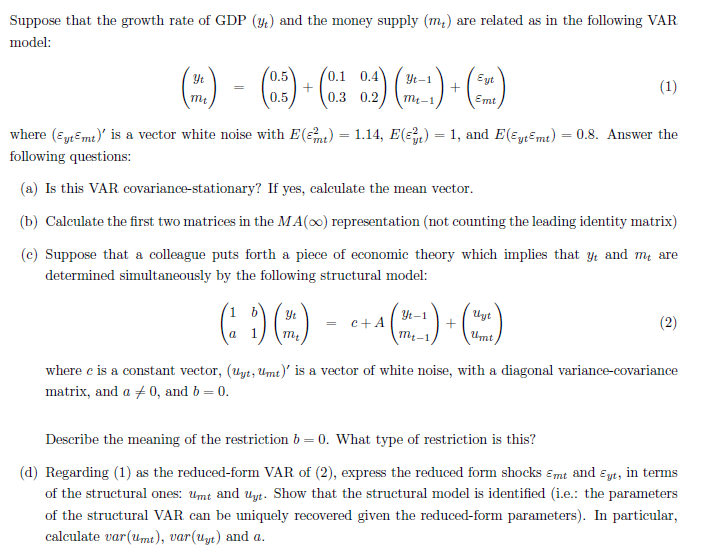

Suppose that the growth rate of GDP (y) and the money supply (m₂) are related as in the following VAR model: Yt-1 Eyt Yt

Posted: Fri Jul 01, 2022 8:14 am

by answerhappygod

- Suppose That The Growth Rate Of Gdp Y And The Money Supply M Are Related As In The Following Var Model Yt 1 Eyt Yt 1 (82.24 KiB) Viewed 30 times

Suppose that the growth rate of GDP (y) and the money supply (m₂) are related as in the following VAR model: Yt-1 Eyt Yt (-) - (0.5) - (0.3 0.2) (-1)+(3) = Emt (1) where (Eytmt)' is a vector white noise with E(mt) = 1.14, E(t) = 1, and E(Eytmt) = 0.8. Answer the following

questions: (a) Is this VAR covariance-stationary? If yes, calculate the mean vector. (b) Calculate the first two matrices in the MA(∞o) representation (not counting the leading identity matrix) (e) Suppose that a colleague puts forth a piece of economic theory which implies that yt and me are determined simultaneously by the following structural model: Yt () () ()+(2) = c+A Umt a where e is a constant vector, (Uyt, Umt)' is a vector of white noise, with a diagonal variance-covariance matrix, and a 0, and b = 0. Describe the meaning of the restriction b=0. What type of restriction is this? (d) Regarding (1) as the reduced-form VAR of (2), express the reduced form shocks Emt and Eyt, in terms of the structural ones: Umt and uyt. Show that the structural model is identified (i.e.: the parameters of the structural VAR can be uniquely recovered given the reduced-form parameters). In particular, calculate var(umt), var(uyt) and a.