Page 1 of 1

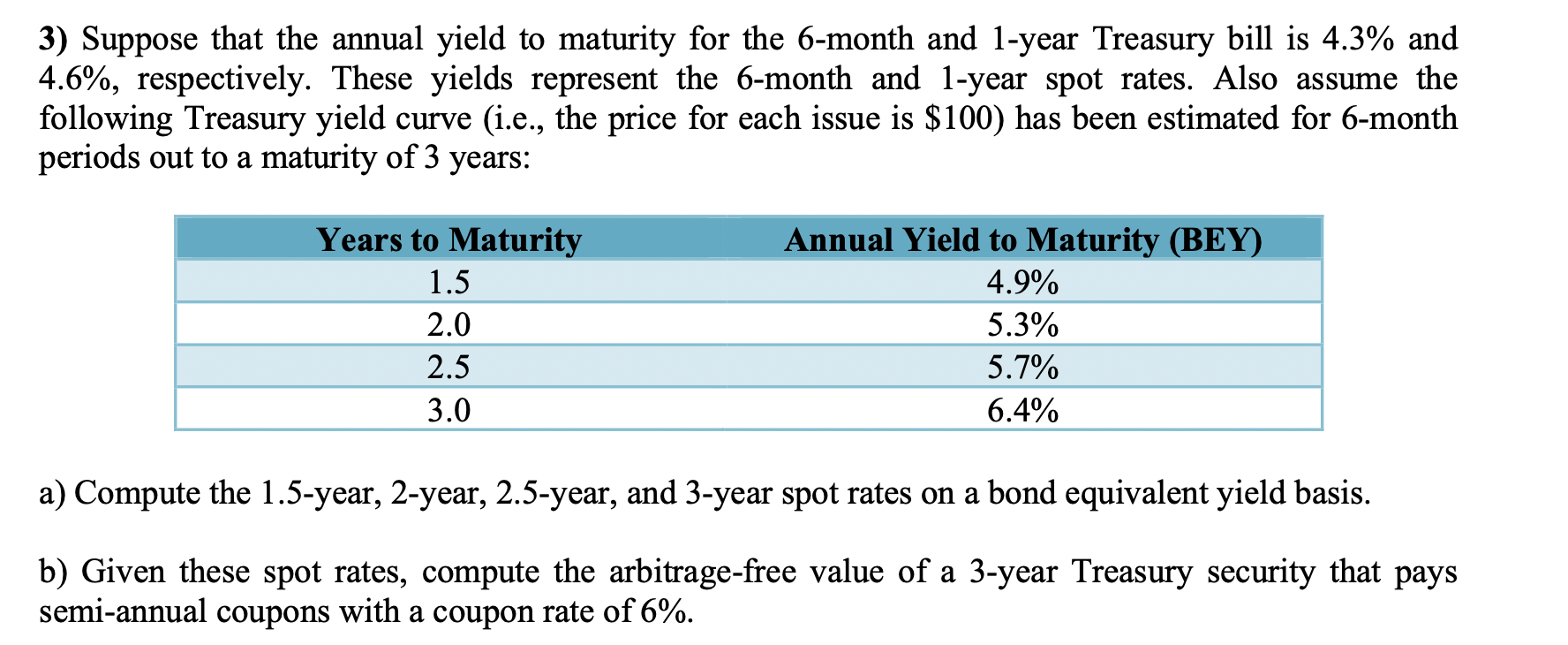

3) Suppose that the annual yield to maturity for the 6-month and 1-year Treasury bill is 4.3% and 4.6%, respectively. Th

Posted: Wed Mar 30, 2022 3:50 pm

by answerhappygod

- 3 Suppose That The Annual Yield To Maturity For The 6 Month And 1 Year Treasury Bill Is 4 3 And 4 6 Respectively Th 1 (342.72 KiB) Viewed 63 times

3) Suppose that the annual yield to maturity for the 6-month and 1-year Treasury bill is 4.3% and 4.6%, respectively. These yields represent the 6-month and 1-year spot rates. Also assume the following Treasury yield curve (i.e., the price for each issue is $100) has been estimated for 6-month periods out to a maturity of 3 years: Years to Maturity 1.5 2.0 2.5 3.0 Annual Yield to Maturity (BEY) 4.9% 5.3% 5.7% 6.4% a) Compute the 1.5-year, 2-year, 2.5-year, and 3-year spot rates on a bond equivalent yield basis. b) Given these spot rates, compute the arbitrage-free value of a 3-year Treasury security that pays semi-annual coupons with a coupon rate of 6%.