Page 1 of 1

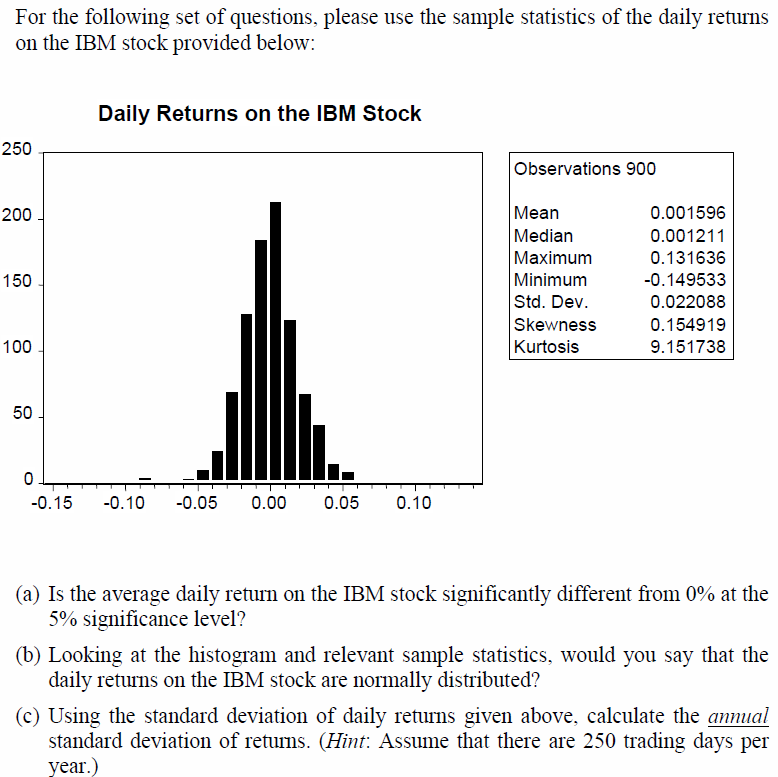

For the following set of questions, please use the sample statistics of the daily returns on the IBM stock provided belo

Posted: Fri Jul 01, 2022 7:46 am

by answerhappygod

- For The Following Set Of Questions Please Use The Sample Statistics Of The Daily Returns On The Ibm Stock Provided Belo 1 (65.62 KiB) Viewed 37 times

For the following set of

questions, please use the sample statistics of the daily returns on the IBM stock provided below: 250 200 150 100 50 Daily Returns on the IBM Stock 0 -0.15 -0.10 -0.05 0.00 0.05 0.10 Observations 900 Mean Median Maximum Minimum Std. Dev. Skewness Kurtosis 0.001596 0.001211 0.131636 -0.149533 0.022088 0.154919 9.151738 (a) Is the average daily return on the IBM stock significantly different from 0% at the 5% significance level? (b) Looking at the histogram and relevant sample statistics, would you say that the daily returns on the IBM stock are normally distributed? (c) Using the standard deviation of daily returns given above, calculate the annual standard deviation of returns. (Hint: Assume that there are 250 trading days per year.)