Page 1 of 1

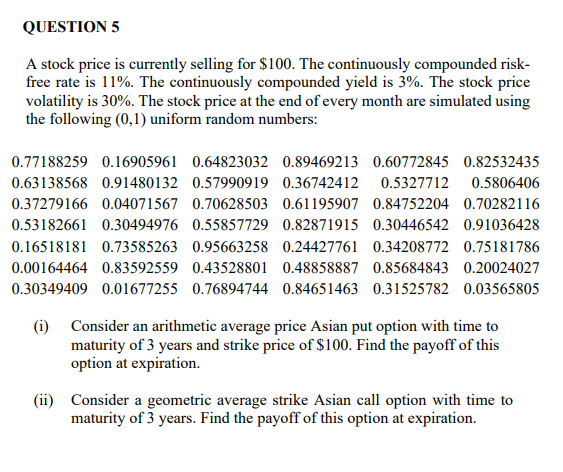

QUESTION 5 A stock price is currently selling for $100. The continuously compounded risk- free rate is 11%. The continuo

Posted: Fri Jul 01, 2022 7:41 am

by answerhappygod

- Question 5 A Stock Price Is Currently Selling For 100 The Continuously Compounded Risk Free Rate Is 11 The Continuo 1 (98.51 KiB) Viewed 28 times

QUESTION 5 A stock price is currently selling for $100. The continuously compounded risk- free rate is 11%. The continuously compounded yield is 3%. The stock price volatility is 30%. The stock price at the end of every month are simulated using the following (0,1) uniform random numbers: 0.77188259 0.16905961 0.64823032 0.89469213 0.60772845 0.82532435 0.63138568 0.91480132 0.57990919 0.36742412 0.5327712 0.5806406 0.37279166 0.04071567 0.70628503 0.61195907 0.84752204 0.70282116 0.53182661 0.30494976 0.55857729 0.82871915 0.30446542 0.91036428 0.16518181 0.73585263 0.95663258 0.24427761 0.34208772 0.75181786 0.00164464 0.83592559 0.43528801 0.48858887 0.85684843 0.20024027 0.30349409 0.01677255 0.76894744 0.84651463 0.31525782 0.03565805 (i) Consider an arithmetic average price Asian put option with time to maturity of 3 years and strike price of $100. Find the payoff of this option at expiration. (ii) Consider a geometric average strike Asian call option with time to maturity of 3 years. Find the payoff of this option at expiration.