Page 1 of 1

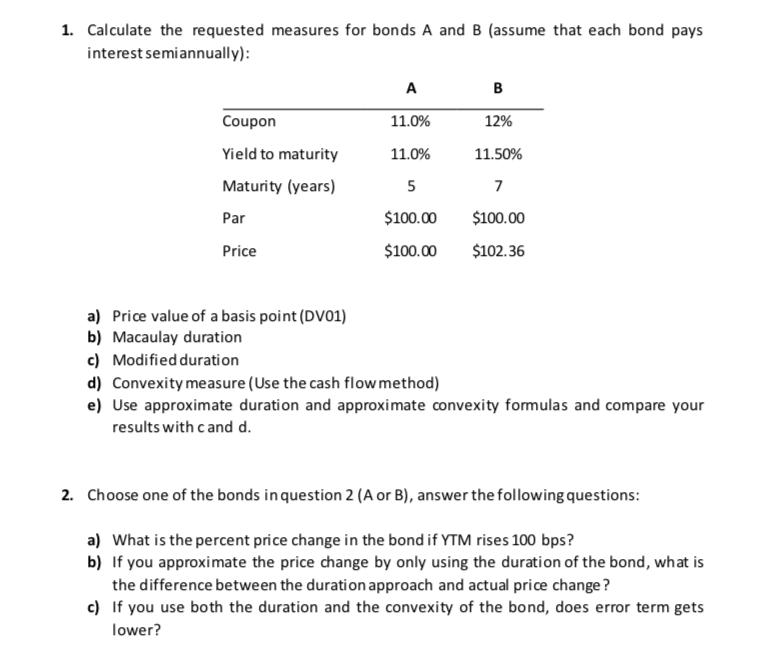

1. Calculate the requested measures for bonds A and B (assume that each bond pays interest semiannually): A B Coupon 11.

Posted: Wed Mar 30, 2022 3:41 pm

by answerhappygod

- 1 Calculate The Requested Measures For Bonds A And B Assume That Each Bond Pays Interest Semiannually A B Coupon 11 1 (69.06 KiB) Viewed 41 times

1. Calculate the requested measures for bonds A and B (assume that each bond pays interest semiannually): A B Coupon 11.0% 12% Yield to maturity 11.0% 11.50% Maturity (years) 5 7 Par $100.00 $100.00 Price $100.00 $102.36 a) Price value of a basis point (DV01) b) Macaulay duration c) Modified duration d) Convexity measure (Use the cash flow method) e) Use approximate duration and approximate convexity formulas and compare your results with cand d. 2. Choose one of the bonds in question 2 (A or B), answer the following questions: a) What is the percent price change in the bond if YTM rises 100 bps? b) If you approximate the price change by only using the duration of the bond, what is the difference between the duration approach and actual price change? c) If you use both the duration and the convexity of the bond, does error term gets lower?