Page 1 of 1

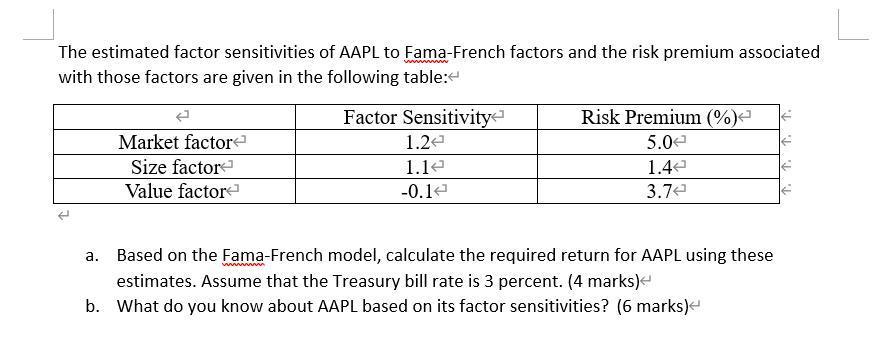

The estimated factor sensitivities of AAPL to Fama-French factors and the risk premium associated with those factors are

Posted: Wed Mar 30, 2022 3:38 pm

by answerhappygod

- The Estimated Factor Sensitivities Of Aapl To Fama French Factors And The Risk Premium Associated With Those Factors Are 1 (48.14 KiB) Viewed 50 times

The estimated factor sensitivities of AAPL to Fama-French factors and the risk premium associated with those factors are given in the following table: T. T Market factor Size factor Value factor Factor Sensitivity 1.24 1.12 -0.14 Risk Premium (% 5.0 1.42 3.72 1. T. a. Based on the Fama-French model, calculate the required return for AAPL using these estimates. Assume that the Treasury bill rate is 3 percent. (4 marks) b. What do you know about AAPL based on its factor sensitivities? (6 marks)