Page 1 of 1

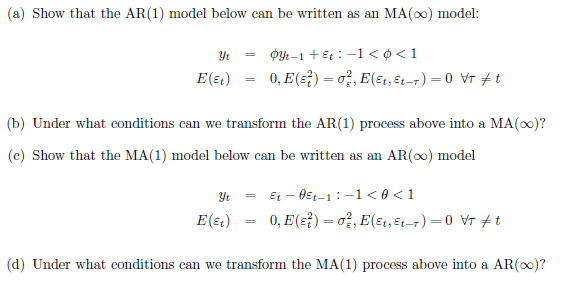

(a) Show that the AR(1) model below can be written as an MA (∞o) model: ¢yt-1 + E : -1<φ<1 0, E() = 0, E(Et, Et-T) = 0 V

Posted: Thu Jun 30, 2022 7:40 pm

by answerhappygod

- 1 (31.31 KiB) Viewed 24 times

(a) Show that the AR(1) model below can be written as an MA (∞o) model: ¢yt-1 + E : -1<φ<1 0, E() = 0, E(Et, Et-T) = 0 VT + t Yt E (et) = (b) Under what conditions can we transform the AR(1) process above into a MA (∞o)? (c) Show that the MA(1) model below can be written as an AR(∞) model Yt E (Et) (d) Under what conditions can we transform the MA(1) process above into a AR(oo)? Et-Et-1-1 < 0 <1 0, E(s) 02, E(Et, Et-T) = 0 VT t = =