Page 1 of 1

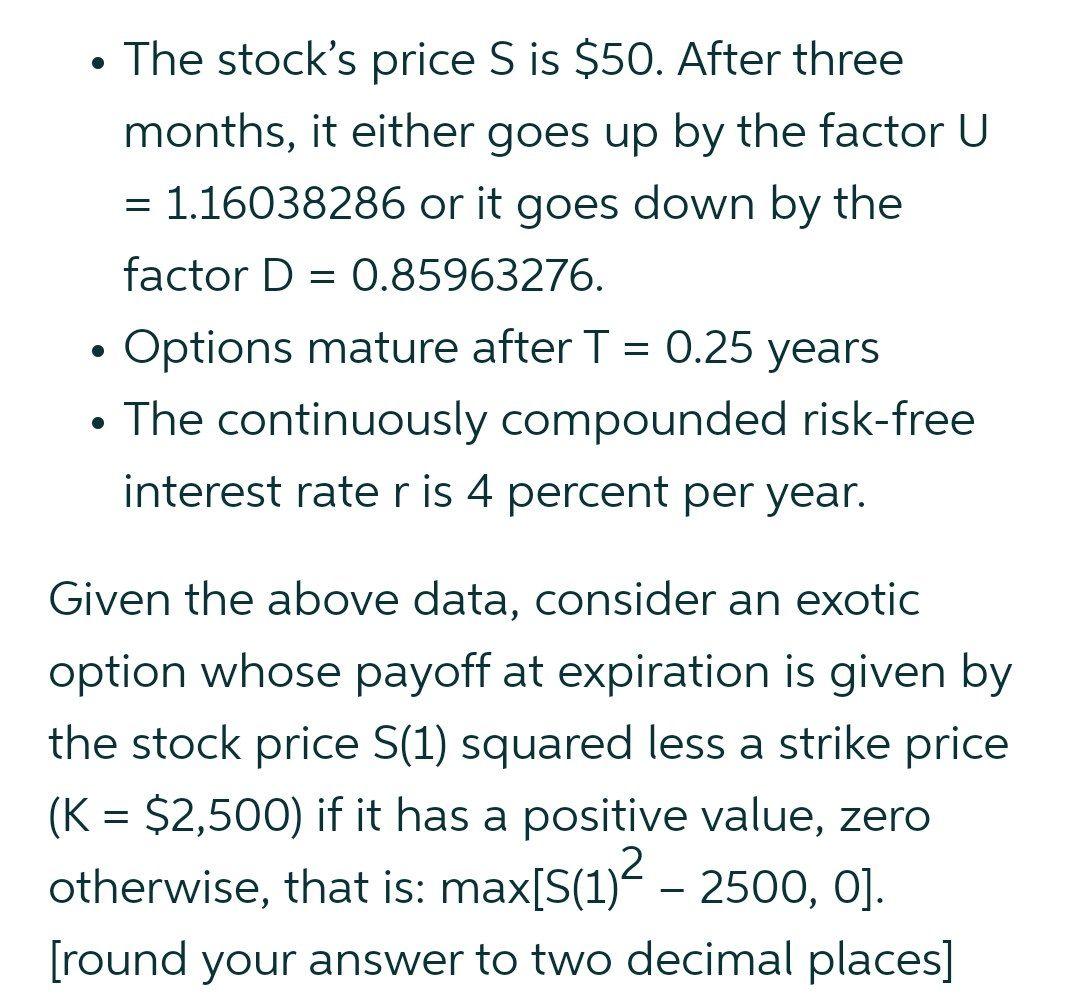

. - The stock's price S is $50. After three months, it either goes up by the factor U = 1.16038286 or it goes down by th

Posted: Mon Mar 21, 2022 4:21 pm

by answerhappygod

- The Stock S Price S Is 50 After Three Months It Either Goes Up By The Factor U 1 16038286 Or It Goes Down By Th 1 (144.19 KiB) Viewed 43 times

. - The stock's price S is $50. After three months, it either goes up by the factor U = 1.16038286 or it goes down by the factor D = 0.85963276. = Options mature after T = 0.25 years • The continuously compounded risk-free interest rate r is 4 percent per year. = Given the above data, consider an exotic option whose payoff at expiration is given by the stock price S(1) squared less a strike price (K = $2,500) if it has a positive value, zero 2 otherwise, that is: max[S(1)2 – 2500, O). 0. [round your answer to two decimal places)