Page 1 of 1

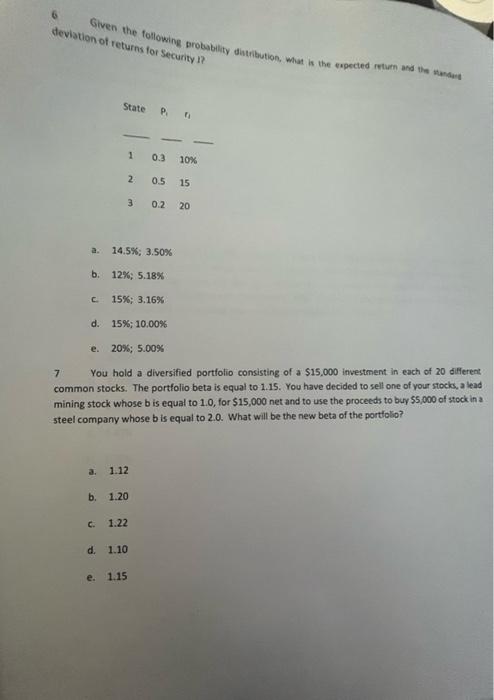

deviation of returns for Security 1? Given the following probability distribution, what is the expected return and the S

Posted: Wed Mar 09, 2022 8:47 am

by answerhappygod

- Deviation Of Returns For Security 1 Given The Following Probability Distribution What Is The Expected Return And The S 1 (22.45 KiB) Viewed 179 times

deviation of returns for Security 1? Given the following probability distribution, what is the expected return and the State P 1 0.3 10% 2 0.5 15 3 0.2 20 a. 14.5%; 3.50% b. 12%, 5.18% C e. 15%; 3.16% d. 15%; 10.00% 20%; 5.00% 7 You hold a diversified portfolio consisting of a $15,000 investment in each of 20 different common stocks. The portfolio beta is equal to 1.15. You have decided to sell one of your stocks, a lead mining stock whose bis equal to 1.0, for $15,000 net and to use the proceeds to buy 55,000 of stock in a steel company whose bis equal to 2.0. What will be the new beta of the portfolio? a 1.12 b. 1.20 C. 1.22 d. 1.10 e. 1.15