Page 1 of 1

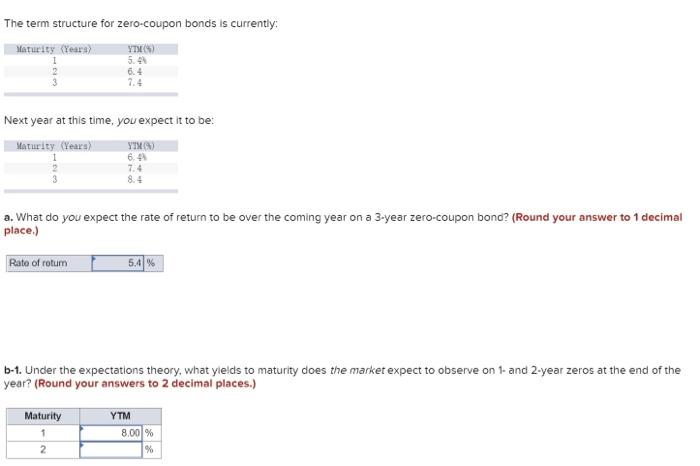

The term structure for zero-coupon bonds is currently: Maturity Years 1 YTHS 5.4 6.4 7.4 Next year at this time, you exp

Posted: Wed Mar 09, 2022 8:34 am

by answerhappygod

- The Term Structure For Zero Coupon Bonds Is Currently Maturity Years 1 Yths 5 4 6 4 7 4 Next Year At This Time You Exp 1 (23.68 KiB) Viewed 45 times

The term structure for zero-coupon bonds is currently: Maturity Years 1 YTHS 5.4 6.4 7.4 Next year at this time, you expect it to be: Maturity Years YTYS 6.4 7.4 8.4 a. What do you expect the rate of return to be over the coming year on a 3-year zero-coupon bond? (Round your answer to 1 decimal place.) Rate of rotum 5.4 % b-1. Under the expectations theory, what ylelds to maturity does the market expect to observe on 1- and 2-year zeros at the end of the year? (Round your answers to 2 decimal places.) Maturity 1 YTM 8.00% % 2