1 point 1 point 1) W(t), t> 0 is Brownian motion then for all 0 = to

Posted: Sat Feb 26, 2022 11:19 am

- 1 Point 1 Point 1 W T T 0 Is Brownian Motion Then For All 0 To T1 Tm E W Tm W Tm 1 Tm Tm 1 Ew Tm 1 (295.12 KiB) Viewed 75 times

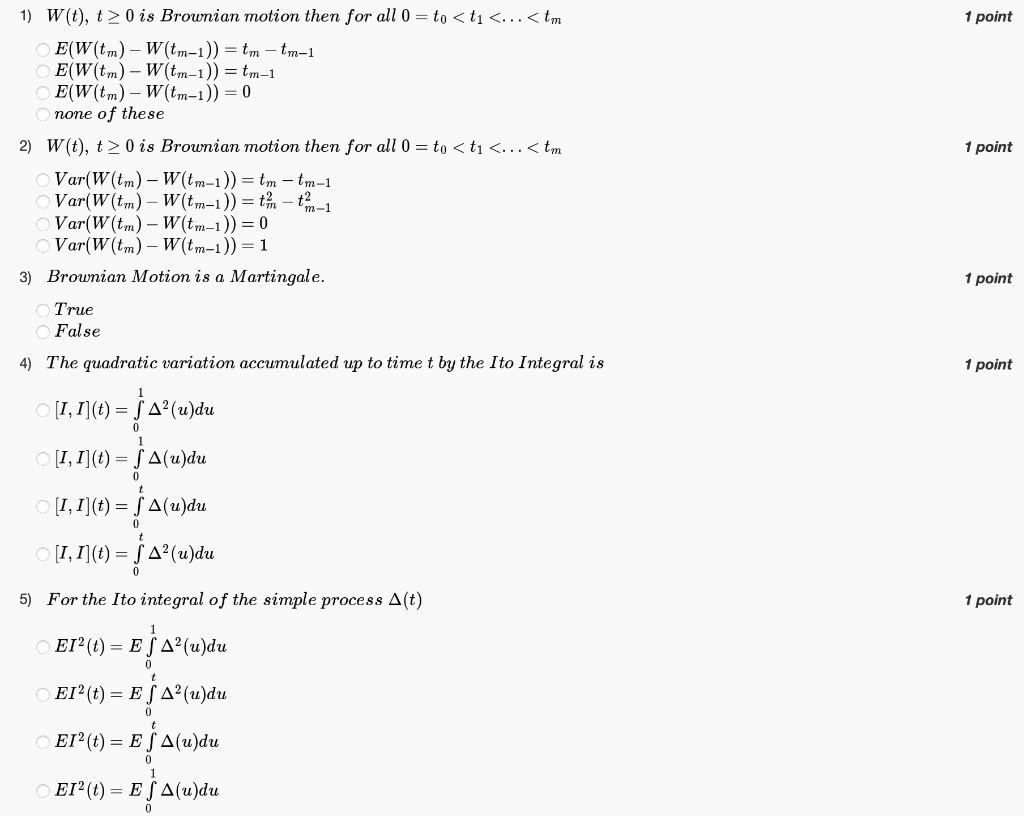

1 point 1 point 1) W(t), t> 0 is Brownian motion then for all 0 = to <t1 <...<tm E(W(tm) - W(tm-1)) = tm - tm-1 EW(tm) - W(tm-1)) = tm-1 EW(tm) - W(tm-1)) = 0 none of these 2) W(t), t > 0 is Brownian motion then for all 0 = to <tı <...<tm Var(W(tm)-W(tm-1)) = tm -tm-1 Var(W(tm) - W(tm-1)) = tm t2 Var(W(tm) - W(tm-1)) = 0 Var(W(tm) - W(tm-1)) = 1 3) Brownian Motion is a Martingale. True False Im-1 1 point 4) The quadratic variation accumulated up to time t by the Ito Integral is 1 point [1,1](t) = A?(u)du 1 [1,1](t) = S A(u)du [1,1](t) = A(u)du [1,1](t) = S A(u)du 5) For the Ito integral of the simple process Alt) 1 point EI?(t) = E SA?(u)du E41 EI?(t) = E S A(u)du EI? (t) = E S A(u)du EI?(t) = E SA(u)du

Posted: Sat Feb 26, 2022 11:19 am

- 1 Point 1 Point 1 W T T 0 Is Brownian Motion Then For All 0 To T1 Tm E W Tm W Tm 1 Tm Tm 1 Ew Tm 1 (295.12 KiB) Viewed 75 times