Page 1 of 1

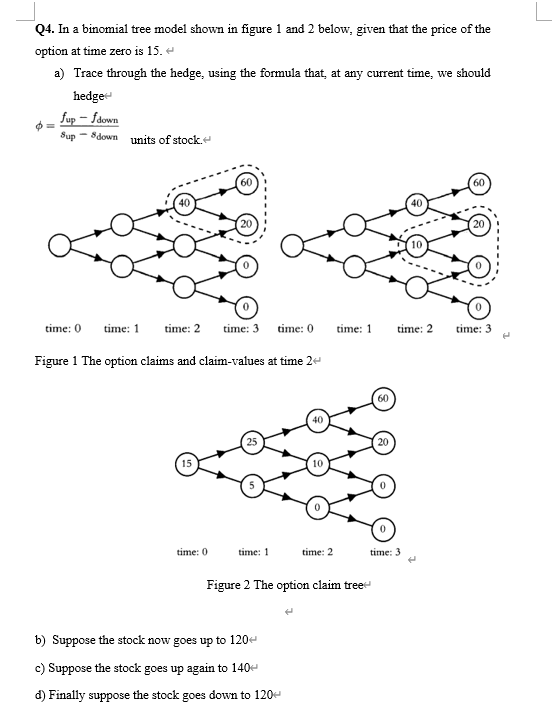

Q4. In a binomial tree model shown in figure 1 and 2 below, given that the price of the option at time zero is 15. a) Tr

Posted: Sat Feb 26, 2022 10:56 am

by answerhappygod

- Q4 In A Binomial Tree Model Shown In Figure 1 And 2 Below Given That The Price Of The Option At Time Zero Is 15 A Tr 1 (59.67 KiB) Viewed 59 times

Q4. In a binomial tree model shown in figure 1 and 2 below, given that the price of the option at time zero is 15. a) Trace through the hedge, using the formula that, at any current time, we should hedge fup - fdown Sup – 8 down units of stock 60 60 40 time: 0 time: 1 time: 2 time: 3 time: 0 time: 1 time: 2 time: 3 Figure 1 The option claims and claim-values at time 24 60 40 20 10 time: 0 time: 1 time: 2 time: 3 Figure 2 The option claim treet b) Suppose the stock now goes up to 120 c) Suppose the stock goes up again to 140- d) Finally suppose the stock goes down to 1204