Page 1 of 1

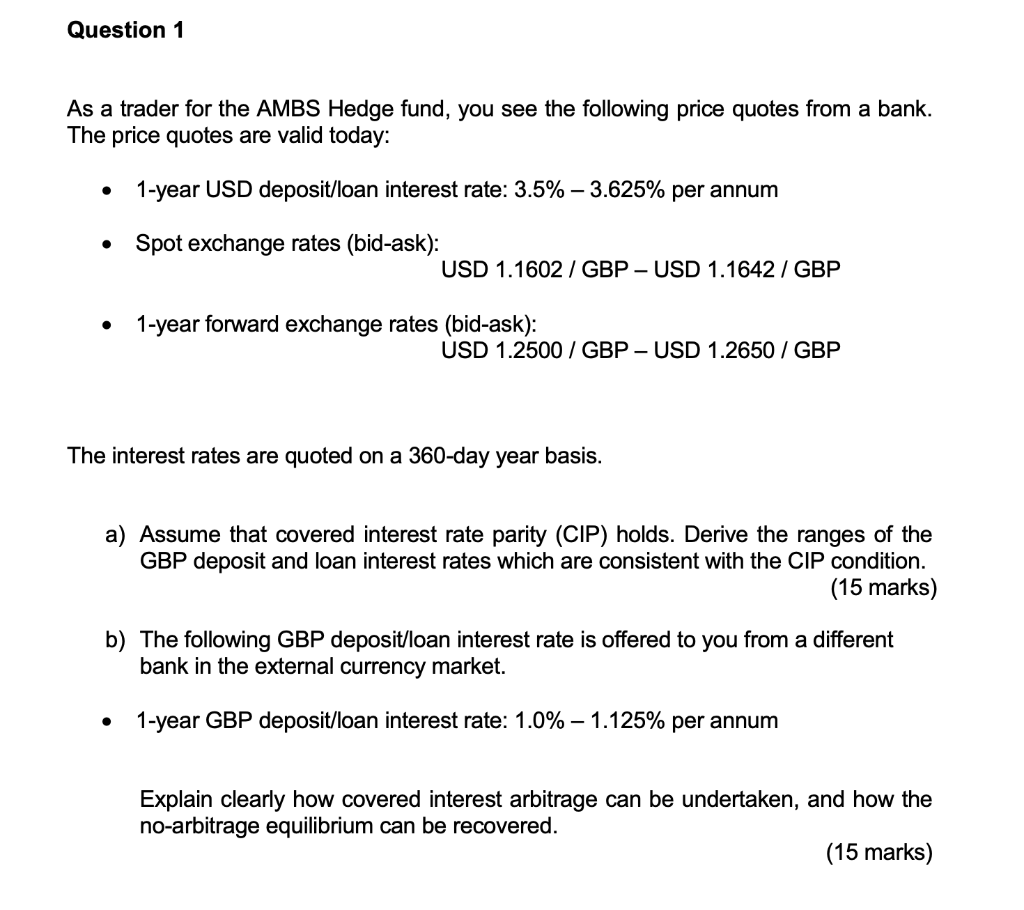

Question 1 As a trader for the AMBS Hedge fund, you see the following price quotes from a bank. The price quotes are val

Posted: Tue Jan 18, 2022 12:59 pm

by answerhappygod

- Question 1 As A Trader For The Ambs Hedge Fund You See The Following Price Quotes From A Bank The Price Quotes Are Val 1 (148.24 KiB) Viewed 77 times

Question 1 As a trader for the AMBS Hedge fund, you see the following price quotes from a bank. The price quotes are valid today: 1-year USD deposit/loan interest rate: 3.5% – 3.625% per annum • Spot exchange rates (bid-ask): USD 1.1602 / GBP - USD 1.1642 / GBP 1-year forward exchange rates (bid-ask): USD 1.2500 / GBP - USD 1.2650 / GBP The interest rates are quoted on a 360-day year basis. a) Assume that covered interest rate parity (CIP) holds. Derive the ranges of the GBP deposit and loan interest rates which are consistent with the CIP condition. (15 marks) b) The following GBP deposit/loan interest rate is offered to you from a different bank in the external currency market. 1-year GBP deposit/loan interest rate: 1.0% – 1.125% per annum Explain clearly how covered interest arbitrage can be undertaken, and how the no-arbitrage equilibrium can be recovered. (15 marks)