Page 1 of 1

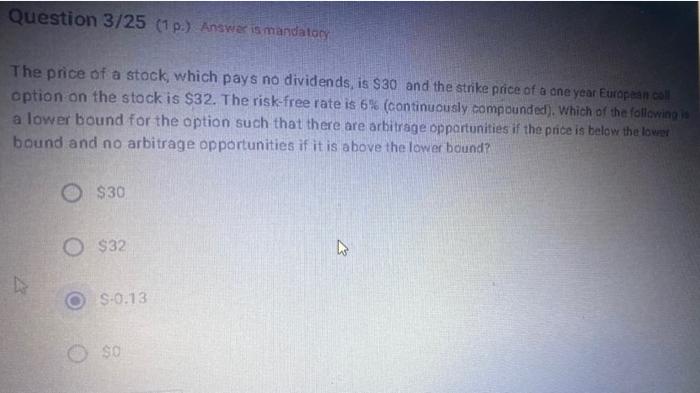

Question 3/25 (1 p.) Answer is mandatory The price of a stock, which pays no dividends, is $30 and the strike price of a

Posted: Tue Jan 18, 2022 12:58 pm

by answerhappygod

- Question 3 25 1 P Answer Is Mandatory The Price Of A Stock Which Pays No Dividends Is 30 And The Strike Price Of A 1 (33.95 KiB) Viewed 61 times

Question 3/25 (1 p.) Answer is mandatory The price of a stock, which pays no dividends, is $30 and the strike price of a one year European coll option on the stock is $32. The risk-free rate is 6% (continuously compounded). Which of the following is a lower bound for the option such that there are arbitrage opportunities if the price is below the lower bound and no arbitrage opportunities if it is above the lower bound? O $30 O $32 Do S:0.13 SO