Page 1 of 1

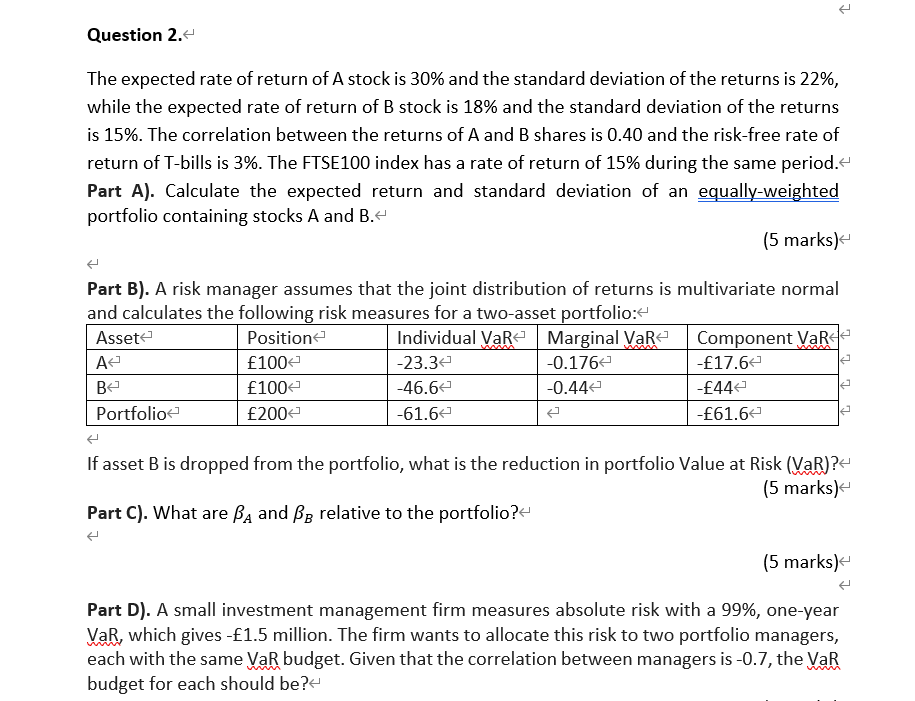

2 Question 2. The expected rate of return of A stock is 30% and the standard deviation of the returns is 22%, while the

Posted: Mon Jan 17, 2022 8:09 am

by answerhappygod

- 2 Question 2 The Expected Rate Of Return Of A Stock Is 30 And The Standard Deviation Of The Returns Is 22 While The 1 (58.17 KiB) Viewed 44 times

2 Question 2. The expected rate of return of A stock is 30% and the standard deviation of the returns is 22%, while the expected rate of return of B stock is 18% and the standard deviation of the returns is 15%. The correlation between the returns of A and B shares is 0.40 and the risk-free rate of return of T-bills is 3%. The FTSE100 index has a rate of return of 15% during the same period. Part A). Calculate the expected return and standard deviation of an equally-weighted portfolio containing stocks A and B. (5 marks) Part B). A risk manager assumes that the joint distribution of returns is multivariate normal and calculates the following risk measures for a two-asset portfolio: Asset Position Individual VaR Marginal VaR Component Var A £1002 -23.34. -0.1762 -£17.6 Be £100 -46.62 -0.44 -£44 Portfolio £2002 -61.62 -£61.6 If asset B is dropped from the portfolio, what is the reduction in portfolio Value at Risk (VaR)?4 (5 marks) Part C). What are BA and BB relative to the portfolio? + (5 marks) Part D). A small investment management firm measures absolute risk with a 99%, one-year VaR, which gives -£1.5 million. The firm wants to allocate this risk to two portfolio managers, each with the same VaR budget. Given that the correlation between managers is -0.7, the VaR budget for each should be?