Page 1 of 1

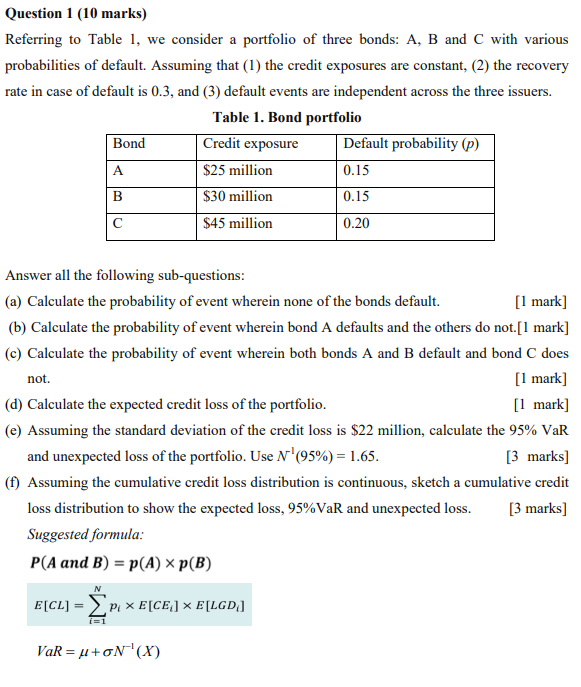

Question 1 (10 marks) Referring to Table 1, we consider a portfolio of three bonds: A, B and C with various probabilitie

Posted: Mon Jan 17, 2022 8:07 am

by answerhappygod

- Question 1 10 Marks Referring To Table 1 We Consider A Portfolio Of Three Bonds A B And C With Various Probabilitie 1 (116.04 KiB) Viewed 78 times

Question 1 (10 marks) Referring to Table 1, we consider a portfolio of three bonds: A, B and C with various probabilities of default. Assuming that (1) the credit exposures are constant, (2) the recovery rate in case of default is 0.3, and (3) default events are independent across the three issuers. Table 1. Bond portfolio Bond Credit exposure Default probability (p) A $25 million 0.15 B $30 million 0.15 с $45 million 0.20 Answer all the following sub-questions: (a) Calculate the probability of event wherein none of the bonds default. [1 mark] (b) Calculate the probability of event wherein bond A defaults and the others do not.[1 mark] (c) Calculate the probability of event wherein both bonds A and B default and bond C does not. [1 mark] (d) Calculate the expected credit loss of the portfolio. [1 mark] (e) Assuming the standard deviation of the credit loss is $22 million, calculate the 95% VaR and unexpected loss of the portfolio. Use N (95%) = 1.65. [3 marks] (f) Assuming the cumulative credit loss distribution is continuous, sketch a cumulative credit loss distribution to show the expected loss, 95%VaR and unexpected loss. [3 marks] Suggested formula: P(A and B) = P(A) * p(B) E[CL] = P. x E[CE] * E[LGD] i=1 VaR = 4+ON-'(X)