Page 1 of 1

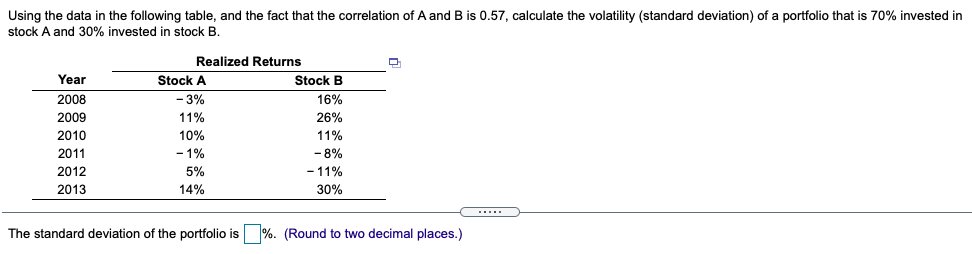

Using the data in the following table, and the fact that the correlation of A and B is 0.57, calculate the volatility (s

Posted: Thu Dec 23, 2021 8:30 am

by answerhappygod

- Using The Data In The Following Table And The Fact That The Correlation Of A And B Is 0 57 Calculate The Volatility S 1 (28.2 KiB) Viewed 109 times

Using the data in the following table, and the fact that the correlation of A and B is 0.57, calculate the volatility (standard deviation) of a portfolio that is 70% invested in stock A and 30% invested in stock B. Year 2008 2009 2010 2011 2012 2013 Realized Returns Stock A Stock B -3% 16% 11% 26% 10% 11% - 1% -8% 5% - 11% 14% 30% The standard deviation of the portfolio is %. (Round to two decimal places.)