Page 1 of 1

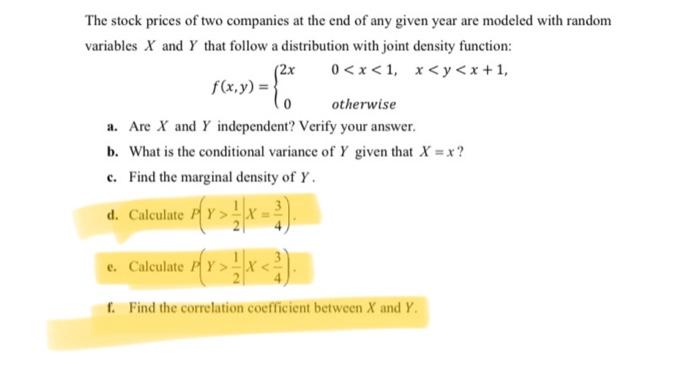

The stock prices of two companies at the end of any given year are modeled with random variables X and Y that follow a d

Posted: Wed Dec 15, 2021 10:29 am

by answerhappygod

- The Stock Prices Of Two Companies At The End Of Any Given Year Are Modeled With Random Variables X And Y That Follow A D 1 (21.93 KiB) Viewed 97 times

The stock prices of two companies at the end of any given year are modeled with random variables X and Y that follow a distribution with joint density function: (2x 0<x<1, x <y <x+1, f(x,y) = 0 otherwise a. Are X and Y independent? Verify your answer. b. What is the conditional variance of Y given that X = x ? c. Find the marginal density of Y. 96.9 - d. Calculate Calculate P{ x >}x<3) 1. Find the correlation coefficient between X and Y.