Page 1 of 1

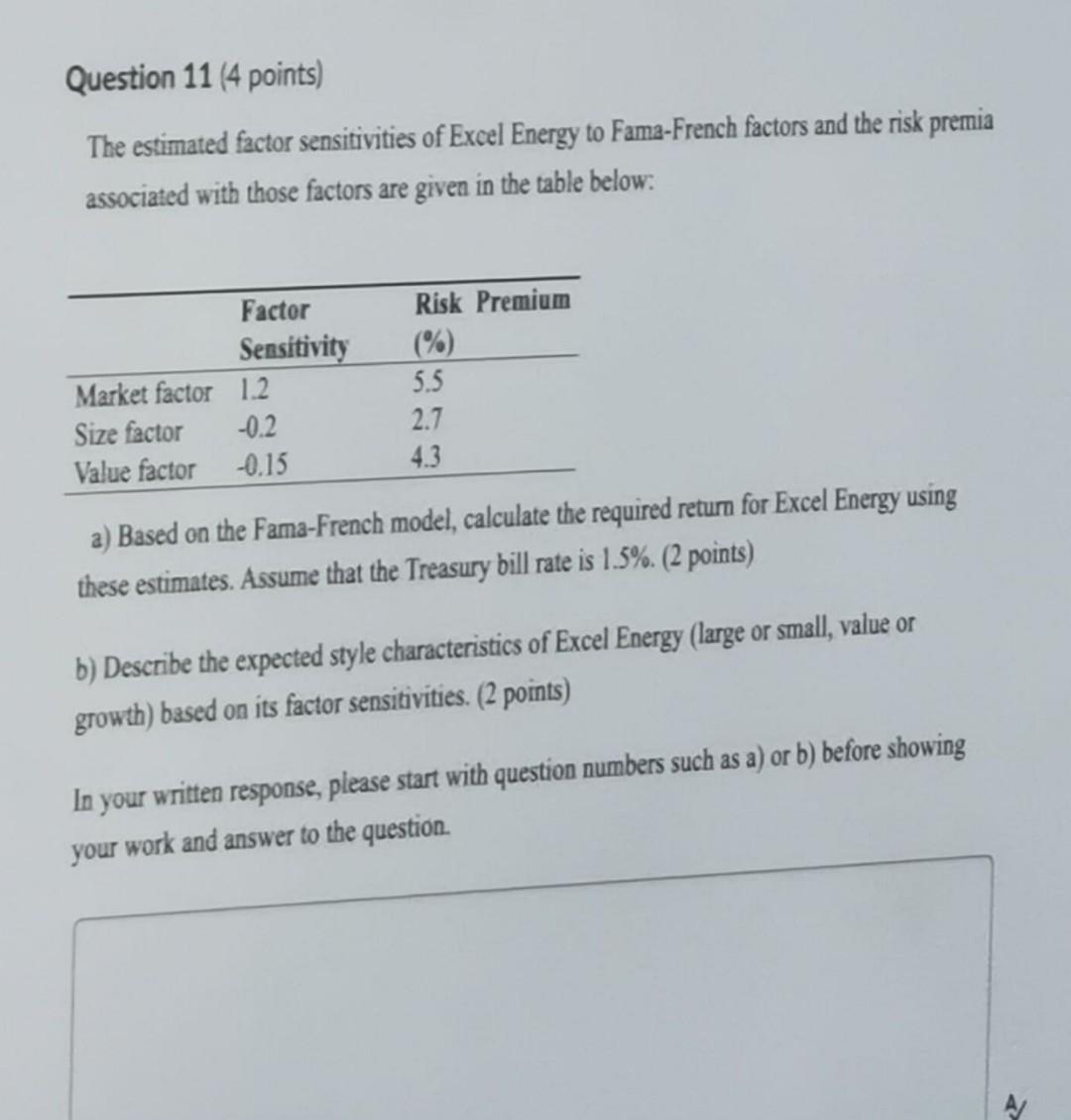

Question 11 (4 points) The estimated factor sensitivities of Excel Energy to Fama-French factors and the risk premia ass

Posted: Mon Jun 06, 2022 7:34 am

by answerhappygod

- Question 11 4 Points The Estimated Factor Sensitivities Of Excel Energy To Fama French Factors And The Risk Premia Ass 1 (64.51 KiB) Viewed 45 times

Question 11 (4 points) The estimated factor sensitivities of Excel Energy to Fama-French factors and the risk premia associated with those factors are given in the table below: Risk Premium Factor Sensitivity (%) Market factor 1.2 5.5 Size factor -0.2 2.7 Value factor -0.15 4.3 a) Based on the Fama-French model, calculate the required return for Excel Energy using these estimates. Assume that the Treasury bill rate is 1.5%. (2 points) b) Describe the expected style characteristics of Excel Energy (large or small, value or growth) based on its factor sensitivities. (2 points) In your written response, please start with question numbers such as a) or b) before showing your work and answer to the question.