Page 1 of 1

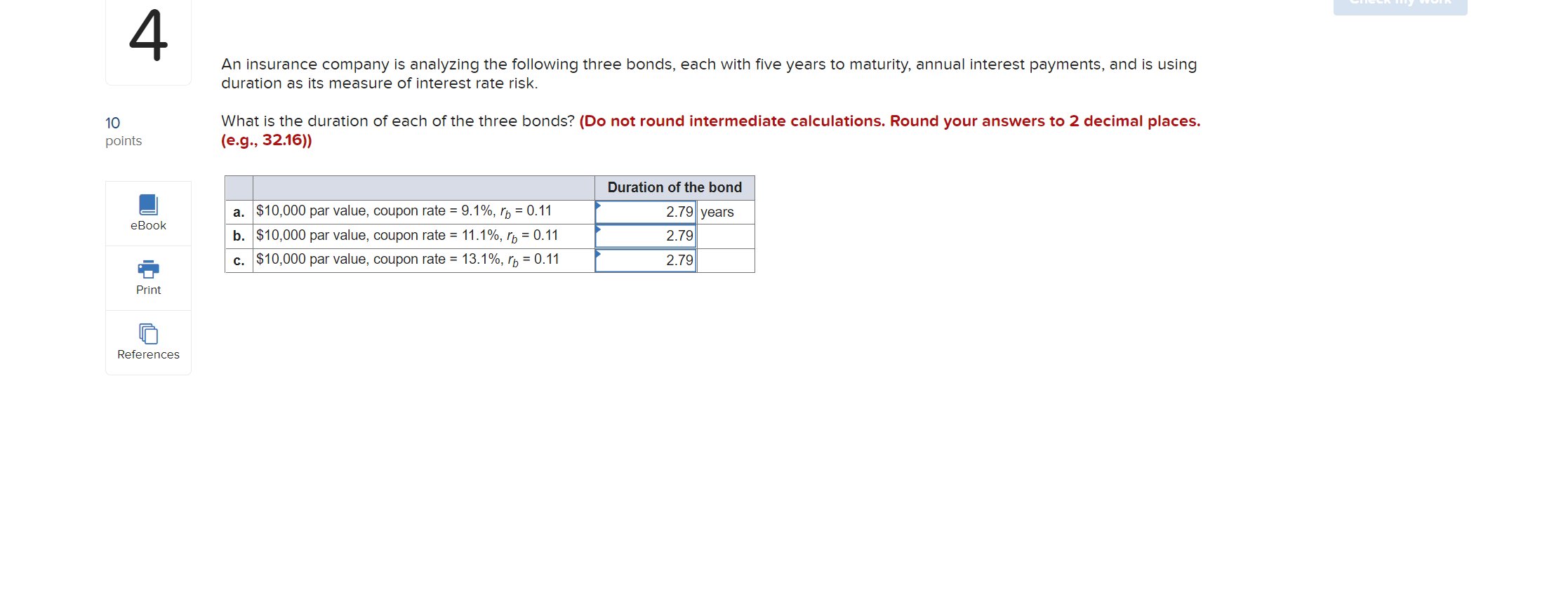

4 An insurance company is analyzing the following three bonds, each with five years to maturity, annual interest payment

Posted: Sun May 29, 2022 5:46 pm

by answerhappygod

- 4 An Insurance Company Is Analyzing The Following Three Bonds Each With Five Years To Maturity Annual Interest Payment 1 (65.71 KiB) Viewed 27 times

4 An insurance company is analyzing the following three bonds, each with five years to maturity, annual interest payments, and is using duration as its measure of interest rate risk. What is the duration of each of the three bonds? (Do not round intermediate calculations. Round your answers to 2 decimal places. (e.g., 32.16)) Duration of the bond a. $10,000 par value, coupon rate = 9.1%, p = 0.11 b. $10,000 par value, coupon rate = 11.1%, p = 0.11 c. $10,000 par value, coupon rate = 13.1%, p = 0.11 2.79 years 2.79 2.79 10 points eBook Print References Sneek my we