Page 1 of 1

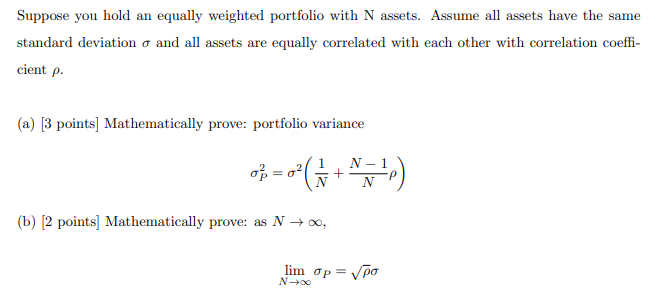

Suppose you hold an equally weighted portfolio with N assets. Assume all assets have the same standard deviation and all

Posted: Sun May 29, 2022 5:02 pm

by answerhappygod

- Suppose You Hold An Equally Weighted Portfolio With N Assets Assume All Assets Have The Same Standard Deviation And All 1 (31.55 KiB) Viewed 35 times

Suppose you hold an equally weighted portfolio with N assets. Assume all assets have the same standard deviation and all assets are equally correlated with each other with correlation coeffi- cient p. (a) [3 points] Mathematically prove: portfolio variance 08-0² (1-10) = + N (b) [2 points] Mathematically prove: as N → ∞, lim op = √po N→∞