Page 1 of 1

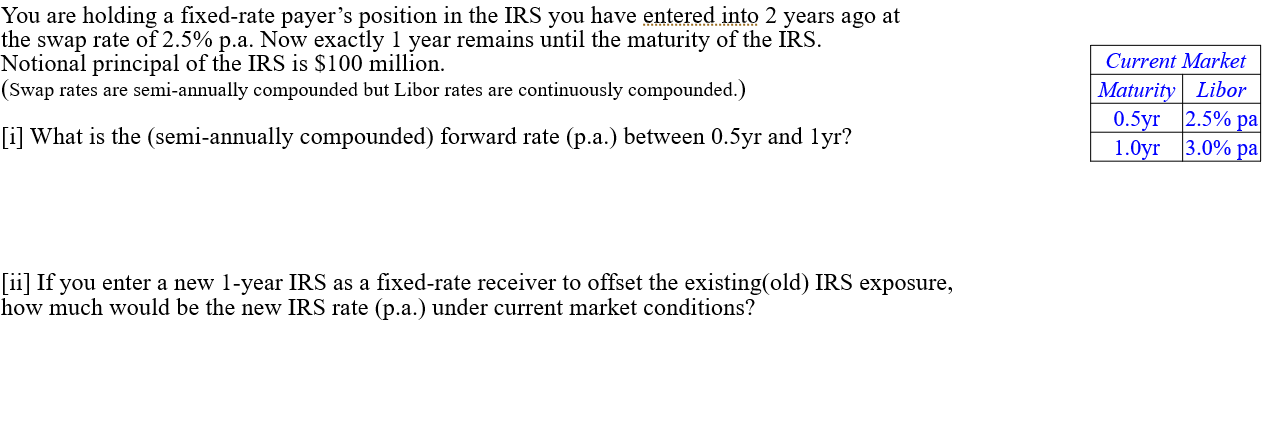

You are holding a fixed-rate payer's position in the IRS you have entered into 2 years ago at the swap rate of 2.5% p.a.

Posted: Sun May 29, 2022 4:37 pm

by answerhappygod

- You Are Holding A Fixed Rate Payer S Position In The Irs You Have Entered Into 2 Years Ago At The Swap Rate Of 2 5 P A 1 (41.82 KiB) Viewed 25 times

You are holding a fixed-rate payer's position in the IRS you have entered into 2 years ago at the swap rate of 2.5% p.a. Now exactly 1 year remains until the maturity of the IRS. Notional principal of the IRS is $100 million. (Swap rates are semi-annually compounded but Libor rates are continuously compounded.)

What is the (semi-annually compounded) forward rate (p.a.) between 0.5yr and lyr? [ii] If you enter a new 1-year IRS as a fixed-rate receiver to offset the existing(old) IRS exposure, how much would be the new IRS rate (p.a.) under current market conditions? Current Market Maturity Libor 0.5yr 2.5% pa 1.0yr 3.0% pa