Page 1 of 1

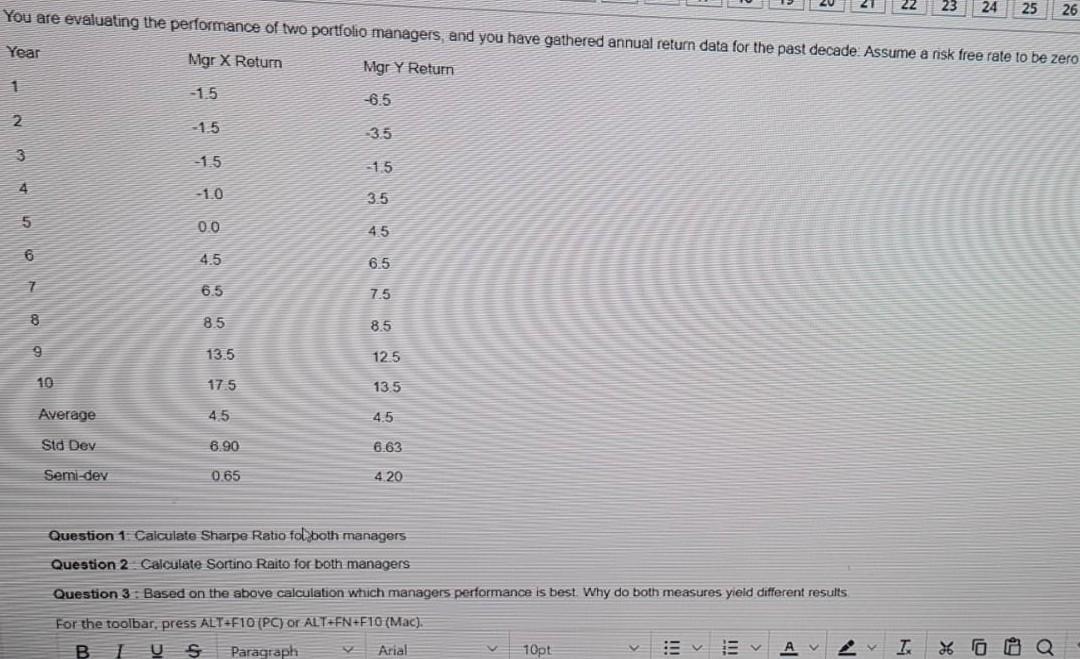

24 25 26 You are evaluating the performance of two portfolio managers, and you have gathered annual return data for the

Posted: Sun May 29, 2022 4:36 pm

by answerhappygod

- 24 25 26 You Are Evaluating The Performance Of Two Portfolio Managers And You Have Gathered Annual Return Data For The 1 (113.67 KiB) Viewed 26 times

24 25 26 You are evaluating the performance of two portfolio managers, and you have gathered annual return data for the past decade. Assume a risk free rate to be zero Year Mgr X Return Mgr Y Return 1 -1.5 -6.5 -1.5 -3.5 -15 -1.5 -1.0 3.5 0.0 45 4.5 6.5 6.5 7.5 8.5 8.5 13.5 12.5 10 17.5 13.5 Average 4.5 4.5 Std Dev 6.90 6.63 Semi-dev 0.65 4.20 Question 1: Calculate Sharpe Ratio fol both managers Question 2 Calculate Sortino Raito for both managers Question 3: Based on the above calculation which managers performance is best. Why do both measures yield different results For the toolbar, press ALT+F10 (PC) or ALT+FN+F10 (Mac). V XQ E E AVVI 10pt BIUS Paragraph Arial 2 3 4 5 6 8 9