Page 1 of 1

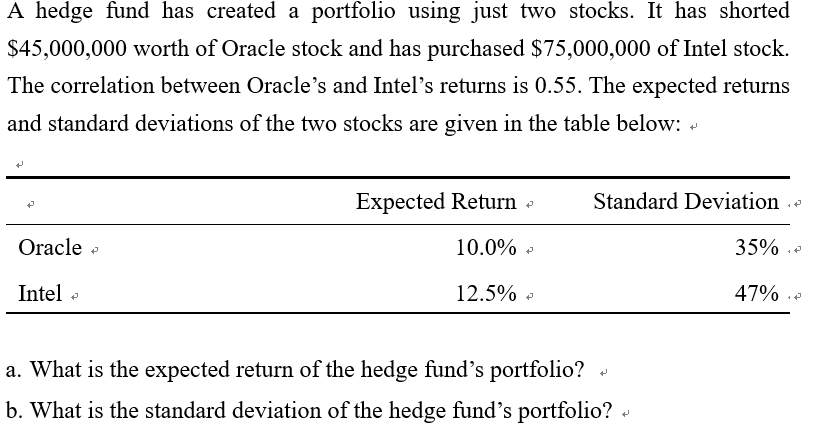

A hedge fund has created a portfolio using just two stocks. It has shorted $45,000,000 worth of Oracle stock and has pur

Posted: Thu May 26, 2022 7:16 am

by answerhappygod

- A Hedge Fund Has Created A Portfolio Using Just Two Stocks It Has Shorted 45 000 000 Worth Of Oracle Stock And Has Pur 1 (34.6 KiB) Viewed 23 times

A hedge fund has created a portfolio using just two stocks. It has shorted $45,000,000 worth of Oracle stock and has purchased $75,000,000 of Intel stock. The correlation between Oracle's and Intel's returns is 0.55. The expected returns and standard deviations of the two stocks are given in the table below: Expected Return - Standard Deviation. + Oracle 10.0% 35%. P Intel 12.5% - 47%. a. What is the expected return of the hedge fund's portfolio? b. What is the standard deviation of the hedge fund's portfolio? → + P